Quick Decision Framework

- Who This Is For: Ecommerce operators, Shopify merchants, and DTC founders who hold AMD stock, track semiconductor market movements, or want to understand what AMD’s AI hardware trajectory means for the infrastructure powering the tools their businesses run on.

- Skip If: You have no exposure to semiconductor stocks and are not evaluating AI infrastructure investments. This is a financial analysis piece, not a product recommendation.

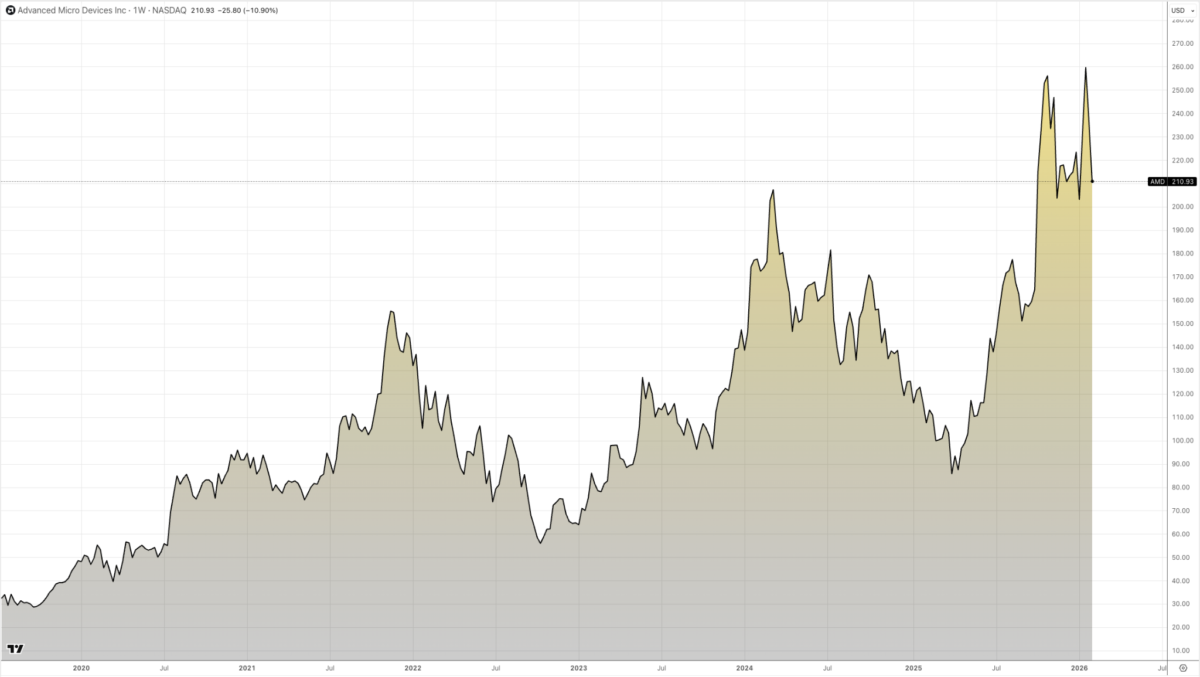

- Key Insight: AMD posted the best quarter in its history and the stock still fell nearly 10%. The selloff was not about the numbers themselves. It was about what was hiding inside them.

- What You’ll Learn: Where AMD’s record revenue actually came from, why Wall Street was not satisfied with a beat-and-raise quarter, and what the Q1 2026 guidance signals about the durability of AMD’s AI growth story.

- Time to Read: 5 minutes.

A record quarter only impresses if the numbers are repeatable. Wall Street did not sell AMD’s results. It sold the question of whether those results can happen again.

What You’ll Learn

- Why AMD’s Q4 2025 results were simultaneously the best in the company’s history and a source of genuine investor concern, and how both things can be true at the same time.

- What the China Instinct shipments and the inventory dynamics inside the quarter actually did to AMD’s reported margins, and why analysts treated them as signals rather than baseline performance.

- How AMD’s four business segments performed individually, which ones are growing sustainably, and which ones are facing structural headwinds heading into 2026.

- What AMD’s Q1 2026 guidance of $9.5 to $10.1 billion implies about the trajectory of the AI hardware business and how to read the sequential revenue step-down in context.

- Why the OpenAI partnership, the Helios rack-scale platform, and the next-generation Xbox chip matter more for AMD’s long-term story than any single quarter’s margin percentage.

A Record Quarter That Still Disappointed

Advanced Micro Devices closed Q4 2025 with the highest revenue and profit in its history. Revenue of $10.27 billion grew 34% year over year. Non-GAAP net income rose 42% to $2.5 billion. GAAP net income jumped 213% to $1.24 billion. Non-GAAP gross margin reached 57%. For the full year, AMD grew revenue 34% to $34.64 billion and increased GAAP net income 164% to $4.34 billion. Every headline number beat consensus estimates. The stock fell nearly 10% the following session.

That reaction is not irrational. It reflects a specific concern about the quality of what drove the beat, and whether the conditions that produced it are repeatable. To understand what actually happened, you have to look past the top-line figures to what was sitting inside them, and then read the Q1 2026 guidance against that context. The day after the report, AMD was among the sharpest single-session decliners on the stock market map of large-cap technology names, even as the broader semiconductor sector held relatively stable. That divergence is the signal worth examining.

What Was Actually Inside the Beat

Two factors contributed to AMD’s Q4 outperformance in ways that analysts flagged as non-recurring. The first was approximately $309 million in Instinct MI308 accelerator shipments to Chinese customers. These were not included in AMD’s original Q4 guidance because of ongoing uncertainty around US export restrictions. The shipments happened, the revenue was real, and it contributed meaningfully to the quarter’s results. But AMD explicitly excluded future China Instinct shipments from its forward guidance, confirming that this revenue source would not repeat at the same scale. A contribution that generates several hundred million dollars in one quarter and then effectively disappears is a pull-forward, not a growth driver.

The second factor was the inventory dynamics that flowed through AMD’s reported margins during the quarter. When inventory reserves set aside in prior periods are released because underlying products sold better than expected, the benefit flows back through as income in the current period. This is standard accounting, but it is also a one-time benefit that inflates the reported margin for the quarter in which it occurs. Institutional investors who stripped out both items saw an underlying gross margin profile that pointed back toward the 54% to 55% range rather than the reported 57%. When the Q1 2026 guidance confirmed margins in that lower range, it validated the concern. The Q4 beat was partly real and partly a function of conditions that will not repeat.

Data Center: The Engine That Has to Keep Running

AMD’s data center segment is the center of gravity for the company’s growth story. In Q4, it generated a record $5.4 billion in revenue, up 39% year over year and above analyst estimates. For the full year 2025, the segment produced $16.6 billion, up 32% from 2024. CEO Lisa Su confirmed on the earnings call that both EPYC server processors and Instinct AI accelerators are in high demand, and she guided for data center revenue growth of more than 60% in 2026.

That 60% growth target is the most consequential number in the entire report. It implies AMD expects data center revenue to approach $27 billion in 2026, which would make it the dominant driver of total company performance by a wide margin. The question investors are asking is whether that target is achievable without the China revenue tailwind that benefited Q4 2025. AMD’s answer points to two things: the expanding OpenAI partnership and the Helios rack-scale platform. OpenAI has committed to large-scale Instinct GPU deployments, and Helios positions AMD to compete for integrated rack-level infrastructure contracts rather than just individual accelerator cards. As with the potential OpenAI IPO, investor and regulatory scrutiny on every detail of that relationship is intense, and both companies are being watched closely for signs that the partnership translates into durable, recurring revenue rather than a headline commitment.

AMD also confirmed that next-generation Instinct accelerators are on track, with the MI350 already ramping in volume and the MI450 on the 2026 roadmap. The product pipeline is credible. The execution question is whether customer deployments scale fast enough to absorb the gap left by reduced China shipments and sustain the growth rate Lisa Su has committed to publicly.

Client and Gaming: Strong Quarter, Known Headwinds Ahead

AMD now reports its client computing and gaming businesses together in a single segment. In Q4, combined revenue reached $3.9 billion, up 37% year over year, with the client portion alone hitting a record $3.1 billion driven by Ryzen processor demand and AMD’s continued push into premium and corporate PC segments. Lisa Su was candid about the global PC market outlook, acknowledging that overall unit volumes are likely to contract in 2026. AMD’s strategy is to offset that headwind by concentrating on higher-priced segments that are less sensitive to commodity memory price increases, capturing more revenue per unit even as total market volume shrinks.

Gaming grew approximately 1.5 times in Q4, driven by both Radeon discrete graphics cards and semi-custom system-on-chip solutions for current-generation consoles. The forward outlook is more complicated. AMD expects semi-custom SOC revenue to decline by a significant double-digit percentage in 2026 as the current console cycle ages and manufacturers reduce orders ahead of next-generation hardware transitions. The next major catalyst for AMD’s gaming business is the chip it is developing for Microsoft’s next-generation Xbox console. Lisa Su confirmed the program is on schedule with a product announcement planned for 2027, but meaningful revenue from that partnership will not arrive until the console launches, likely in 2027 or 2028. The gap between the current cycle winding down and the next cycle ramping is a known, quantified headwind that AMD will need to absorb through data center growth.

Embedded: Still Working Through the Correction

The embedded segment, inherited from AMD’s acquisition of Xilinx, continued to underperform relative to the rest of the business. Q4 revenue of $950 million represented only 3% year-over-year growth, and full-year 2025 embedded revenue of $3.5 billion was actually down 3% from 2024. AMD attributes this to customers working through elevated inventory levels built up during the supply chain disruptions of 2022 and 2023. The embedded business serves industrial, automotive, and communications markets where design cycles are long and inventory corrections tend to resolve slowly. AMD has guided for a return to growth in this segment as customer inventory normalizes, but the timeline has repeatedly extended further than initial estimates. At $3.5 billion annually, embedded is not large enough to move the needle on total company results, but its continued underperformance does represent a drag on the overall growth rate.

Reading the Q1 2026 Guidance Correctly

For Q1 2026, AMD guided revenue of $9.5 to $10.1 billion, implying a midpoint of $9.8 billion. That represents approximately 32% year-over-year growth, which is strong in absolute terms for a company at AMD’s scale. It also represents a 5% sequential decline from Q4’s $10.27 billion, which AMD attributes to seasonal factors in the client computing business and the absence of the China Instinct shipments that benefited the prior quarter.

The sequential step-down is explainable. The more important signal is that the Q1 guidance confirmed what the bears suspected after stripping out the non-recurring items: the underlying business is growing at roughly 32% year over year with margins in the 54% to 55% range, not the 57% that Q4 reported. That is still a genuinely strong result. The problem is that the stock had been priced for something better, and the guidance reset those expectations in a single session.

AMD’s management is not abandoning its strategic targets. Lisa Su framed 2025 as a defining year and confirmed the company is entering 2026 with accelerating demand for EPYC, Ryzen, and AI server solutions that is already outpacing supply in some configurations. The five-year goal of growing total revenue by more than 35% annually remains intact. Achieving it from a $34.64 billion base requires the data center business to deliver on its 60% growth guidance, and it requires the OpenAI partnership and Helios platform to generate revenue at scale rather than remaining a pipeline story. Those are meaningful execution requirements, and they are what investors will be watching across every quarter of 2026.

Frequently Asked Questions

Why did AMD’s stock fall after reporting record profits?

The market’s reaction reflected concern about the quality of the earnings beat rather than the headline numbers. Two factors contributed to AMD’s Q4 outperformance in ways that analysts flagged as non-recurring: approximately $309 million in Instinct MI308 GPU sales to Chinese customers that AMD confirmed would not repeat at the same scale going forward, and inventory dynamics that provided a one-time margin benefit during the quarter. Stripping out both items, AMD’s underlying gross margin pointed back toward the 54% to 55% range rather than the reported 57%. When Q1 2026 guidance confirmed margins in that lower range alongside a sequential revenue decline, institutional investors concluded that the Q4 beat was partly a one-time event and adjusted their positions accordingly. The stock had also run significantly ahead of the earnings report, leaving limited room for any guidance disappointment.

What is AMD’s data center business and why does it matter?

AMD’s data center segment sells two primary product lines: EPYC server processors, which compete with Intel’s Xeon CPUs for enterprise and cloud server workloads, and Instinct AI accelerators, which compete with Nvidia’s H100 and B200 GPUs for AI training and inference workloads. In Q4 2025, the segment generated $5.4 billion in revenue, up 39% year over year, making it AMD’s largest and fastest-growing business. For the full year, it produced $16.6 billion. AMD has guided for data center revenue growth of more than 60% in 2026, which would push the segment toward $27 billion and make it the primary driver of total company performance. The segment’s growth depends on continued EPYC server share gains against Intel and on expanding Instinct GPU deployments at hyperscalers and AI companies including OpenAI.

What is the Helios platform and why is AMD talking about it?

Helios is AMD’s rack-scale AI infrastructure platform, designed to compete for large-scale AI deployments that require integrated systems rather than individual accelerator cards. As AI workloads grow in complexity and scale, hyperscalers and large AI companies increasingly want to purchase complete rack-level solutions that include networking, cooling, and power management alongside the compute hardware. Nvidia has been the dominant supplier of these integrated systems, which command higher margins and create stronger customer lock-in than component sales. AMD’s Helios platform is its strategic response to that market shift, positioning the company to capture a larger share of total infrastructure spend rather than just the GPU component. Early customer conversations, including the OpenAI partnership, are expected to validate the platform’s commercial viability across 2026.

What does AMD’s gaming business look like going into 2026?

AMD’s gaming segment faces a known structural headwind in 2026. The current generation of major gaming consoles uses AMD semi-custom system-on-chip solutions, and AMD has confirmed that semi-custom SOC revenue will decline by a significant double-digit percentage this year as console manufacturers reduce orders ahead of next-generation hardware transitions. On the discrete graphics card side, AMD’s Radeon business continues to compete with Nvidia in the consumer GPU market, though Nvidia maintains dominant market share at the high end. The next major catalyst for AMD’s gaming business is the next-generation Microsoft Xbox console, for which AMD is developing the primary chip as part of a multi-year partnership that also covers server infrastructure for Xbox Cloud Gaming. Lisa Su confirmed the program is on schedule with a product announcement expected in 2027.

How should ecommerce operators think about AMD’s results?

For Shopify merchants and DTC operators, AMD’s earnings matter in two practical ways. First, if you hold AMD stock or have exposure through index funds, understanding the quality-of-earnings debate helps you read the post-earnings decline as a valuation reset rather than a sign of operational deterioration. The underlying business is genuinely strong. Second, AMD’s AI hardware growth story is directly connected to the infrastructure that powers the AI tools ecommerce operators use every day, from inventory forecasting to customer service automation to personalization engines. The pace at which AMD and its competitors scale AI compute capacity affects how quickly those tools improve and how accessible they become to merchants at every revenue level. AMD’s 60% data center growth guidance for 2026, if achieved, signals continued acceleration in AI infrastructure investment that benefits the entire ecosystem of tools built on top of it.