Debt can feel like being stuck in quicksand—the more you fight it, the deeper you sink.

It often starts small but snowballs fast into a huge financial weight on your shoulders before you know it. Explore through the top 10 common mistakes that land people deep in debt. More importantly, we’ll discuss how to sidestep or address these pitfalls before it’s too late.

Understanding exactly where people tend to go wrong can catch any issues early and turn things around. Knowledge is power when it comes to avoiding debt quicksand. Nobody wants to keep struggling to stay afloat. Let’s uncover the hidden traps that can bury your finances if you need to be more careful. By working together, we’ve got this! Let’s get started!

Living beyond your means by overspending on credit cards, taking out excessive loans, and buying things you can’t truly afford is a surefire path to financial ruin. A survey found that 69% of overspending on non-essential purchases is the number one contributor to consumer debt.

Many get caught in the dangerous cycle of spending more than they earn to uphold an unsustainable lifestyle. This accumulates massive balances on high-interest credit cards and predatory personal loans to maintain appearances and current spending levels.

Are you trying to fix these issues? Create a realistic budget aligned with your net income and re-evaluate your priorities. Apps like Budget Planner can help you easily track your cash flow across categories so you can identify areas of habitual overspending to cut back. Consider downgrading your lifestyle, housing, vehicles, dining out, and entertainment to free up cash flow for true priorities.

Live below your means to enable saving. Only buy what you can comfortably afford with cash on hand. It takes practice to override instant gratification and conscious dedication to separate needs versus wants, but doing so prevents you from digging a financial hole.

Life inevitably throws curveballs like sudden unemployment, major car repairs, and medical issues. These unexpected bankruptcies become magnified without cash reserves to weather the storm. A Federal Reserve study found that 58% of Americans have less than $400 in easily accessible emergency savings, leaving them highly vulnerable to any disruption in income.

For example, how long would it take you to pay all the bills without accumulating debt if you lost your job?

Build your rainy day fund with even small, regular contributions to a high-yield savings account. Consistency and patience are key to treating savings contributions like any other non-negotiable expense in your budget. Even $25 or $50 per paycheck adds up over time.

Having 3-6 months’ worth of living expenses available provides tremendous peace of mind and flexibility to handle unexpected expenses without resorting to debt. An emergency fund helps ensure temporary setbacks don’t become financial catastrophes and provides the foundation to pivot and pursue new opportunities.

Numerous pitfalls can lead to accumulating debt, from overspending to neglecting budgeting and savings. One effective solution to address this issue is utilizing text for money services. One effective solution to address this issue is using services. By leveraging convenient text-based platforms for financial management, individuals can set up alerts for their spending, track expenses in real-time, and receive reminders for bill payments.

Credit card companies love minimum payments; they maximize interest income without making a meaningful dent in reducing the actual principal owed. This prolongs the debt repayment period and results in consumers paying far more overall interest charges.

Making minimum payments keeps balances perpetually high and burdens consumers with hefty interest fees over the long run. A better strategy is implementing the debt avalanche or snowball repayment method to target credit card balances methodically.

If you need support getting out of credit card debt, reputable professional solutions around South Carolina can also provide customized guidance. South Carolina debt relief programs offer various avenues to its residents facing financial challenges. One standard option is debt settlement, where negotiations are made with creditors to settle debts for less than the total amount owed.

The debt avalanche approach dictates paying off the card with the highest interest rate first while making minimums on the other cards. This saves the most in interest payments over time compared to other methods. The debt snowball method prioritizes paying off the card with the smallest overall balance first, then rolling that payment amount into the next smallest balance when the first card is paid off. This creates quick motivational wins to keep the momentum going.

The avalanche or snowball method alleviates credit card debt far more efficiently than making minimum payments alone. For optimal results, automate paying at least 10% or more above the minimum amount each month to chip away at balances.

Unpaid debts don’t disappear if ignored; they shift into more threatening territory with debt collectors. Collection agencies may institute wage garnishment, file lawsuits, or tank your credit score if you avoid communication. As unpleasant as it may seem, engaging openly with collectors provides opportunities to negotiate alternative repayment plans, settlements, or dismissal of contested debts.

Document all agreements in writing and know your rights under the Fair Debt Collection Practices Act. Ignoring legitimate debts only cedes control of the situation.

When looking to finance a big purchase like a home, car, or education or consolidate existing high-interest debts, borrowers often accept the first loan offer that comes their way. This frequently results in overpaying and becoming stuck with a burdensome high interest rate.

According to a study, the average interest rate on a personal loan from a bank is 10.63%. However, rates can vary dramatically between lenders. Online lending marketplaces let you easily compare personalized rates from multiple competing companies. While it takes more upfront effort than just accepting the first loan offer, shopping around pays dividends.

As per data, borrowers who compare rates from five lenders save an average of $1,500 over the loan term by choosing the lowest interest option. This assumes a $10,000 loan paid off over 3 years. Sometimes, the savings can exceed $5,000 on larger loans with wider rate variance.

Never accept a high-interest loan, credit card, or line of credit due to urgency or convenience. The short-term relief of quickly accessible funds can cost you dearly over time if you overlook better rates. Be willing to put in the work upfront to submit multiple applications and thoroughly compare all terms and fees. When you need funds, an hour or two of rate shopping could save thousands down the road.

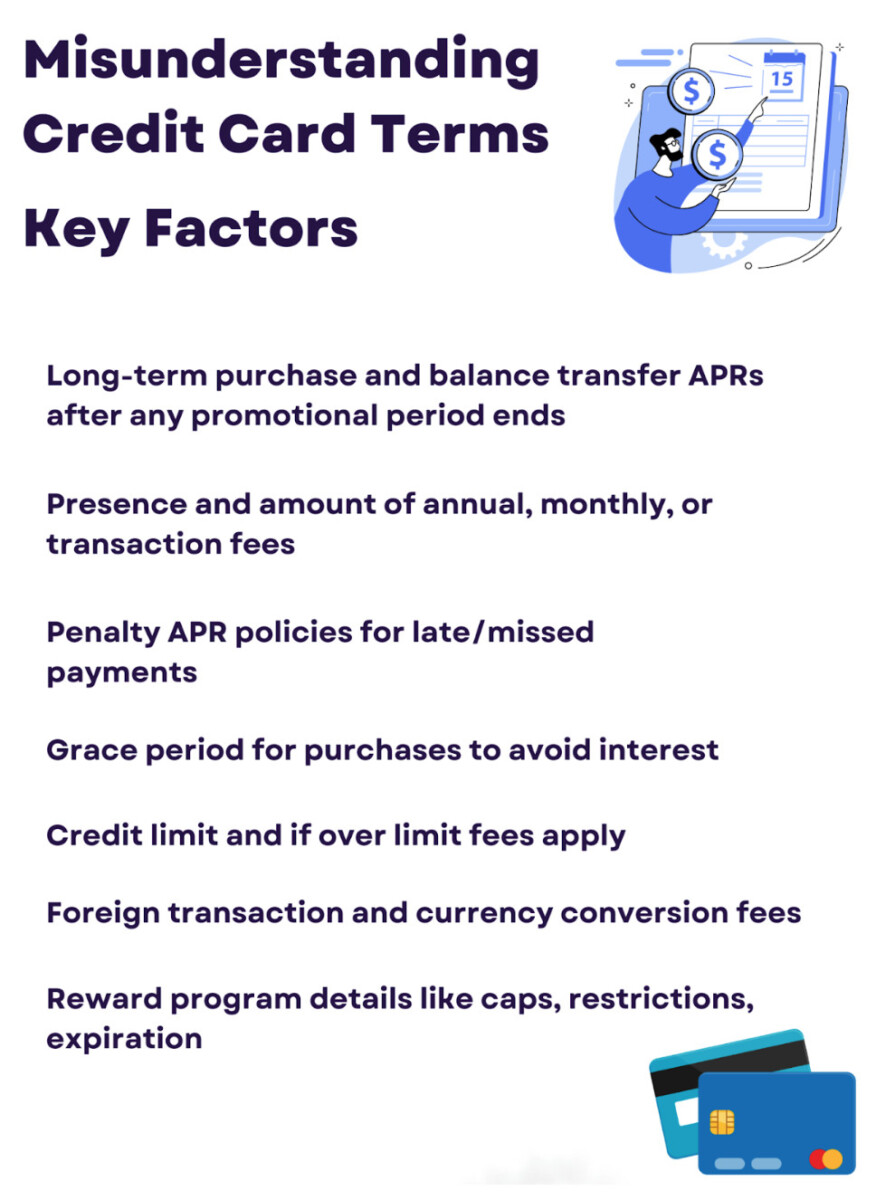

Reading through credit card agreements can be tedious, but failing to understand the fine print and improperly assessing the actual costs is a common and costly mistake. Issuers rely on cardholders skimming contracts and overlooking key terms that can seriously

For example, teaser introductory offers of 0% APR for 12-18 months are enticing. However, missing that a 25% variable rate kicks in after the intro period means suddenly owing substantial interest charges. Likewise, a card may tout no annual fee but have high penalty fees for late payments or over-limit charges.

Burying steep currency conversion fees or APR hikes for even one missed payment in lengthy terms leaves borrowers vulnerable to unexpected expenses and interest costs. Complex reward program details, restrictions, and redemption rules also lead to disappointment.

Thoroughly reviewing all disclosures instead of simply accepting agreements saves money and headaches. Compare critical factors like:

Never sign a credit card agreement you don’t fully grasp. Instead of skimming, read carefully or consult an expert like a financial advisor to decipher unclear or questionable terms. It takes diligence, but an informed understanding of card costs and policy details prevents misunderstandings that drain your wallet.

The allure of credit card rewards programs like cash back, airline miles, and points is simple – who doesn’t like getting something for nothing? However, chasing rewards can quickly backfire if you carry balances and accrue interest charges that outweigh the value of any perks earned.

With attractive sign-up bonuses and enticing ongoing reward structures, issuers incentivize customers to spend more on their cards. But rewards are negated if you can’t pay off statement balances in full each month. For example, if you earn 2% cash back but have a 19% APR, overspending to get rewards costs you far more interest than you gain back.

Before pursuing a rewards card, establish an emergency fund and a budget that allows you to pay the bill each month comfortably. Track your spending diligently to avoid unauthorized overspending. Set up automatic payments for the entire statement balance so you never miss a payment and trigger penalty rates.

Consider rewards a nice bonus rather than a strategy. Weighing lower-rate non-rewards or debit cards may be a better daily spending option to avoid temptation and excessive balances. Use cards only for budgeted purchases you can afford with cash if needed.

Rewards can provide great perks if used strategically and diligently. But the short-term thrill of accruing points and miles never outweighs long-term financial damage from burdensome high-interest credit card debt. Avoid this trap by spending responsibly within your means.

As financial products increase complexity, declining financial literacy fuels poor borrowing and money management decisions. According to the National Financial Capability Study, only 26% of adults could correctly answer basic questions on calculating interest rates, inflation’s

This lack of understanding prevents many individuals from engaging in sound financial behaviors. For example, individuals with lower financial literacy are less likely to plan for retirement, more likely to use high-cost borrowing methods, and more prone to making rash decisions when markets become volatile. They often lack the fundamental knowledge to manage credit and budget effectively, evaluate investment options, and steer clear of predatory financial products.

Boosting your financial knowledge pays enormous dividends across all aspects of your economic life. Read reputable personal finance books, take community college courses, listen to financial podcasts, watch explanatory YouTube videos, and meet with an unbiased monetary advisor to better grasp topics like:

A solid financial education empowers you to make wise borrowing, saving, and spending decisions aligned with your goals and risk tolerance. It helps prevent you from falling prey to dangerous debt traps and guides you in building long-term wealth. Don’t wait – invest in ramping up your financial literacy today.

Co-signing a loan for a family member or friend going through a challenging financial situation may be doing them a favor. However, it comes with serious financial risks that many co-signers overlook in their desire to help.

You become equally liable for the loan payments alongside the primary borrower by co-signing. If they cannot make the payments, this legal responsibility falls entirely on you. Even if they do pay on time, having the co-signed loan debt on your credit record can indirectly jeopardize you in other ways.

Before ever co-signing, have an honest conversation with the borrower about why they need your support and assess your ability to afford the payments if required independently. Consider alternative ways to assist them that don’t put your creditworthiness at risk, like gifting money toward a down payment instead of co-signing a mortgage.

If you still decide to co-sign, negotiate upfront what happens if they default and put all agreements in writing. Set up account access and alerts so you can monitor the status and have time to take action before falling behind. With careful thought and planning, you can help someone in need while protecting your financial standing.

Finally, living paycheck to paycheck without planning paves a risky path even without current debt. There needs to be more retirement savings or a lack of college savings funds for children to set the stage for future shortfalls. Use retirement calculators to estimate the protection necessary to maintain your lifestyle and contribute at least enough to get complete employer matching (if offered).

According to the Employee Benefit Research Institute’s (EBRI) Retirement Confidence Survey, many Americans must adequately plan for their retirement years, leading to financial hardship later in life.

For college, explore tax-advantaged 529 savings plans. Tax-advantaged 529 savings plans are investment accounts designed specifically for educational expenses. These plans give families a powerful tool to save for their children’s education while enjoying significant tax benefits. Even with modest monthly contributions, starting early lets compound interest work magic.

While missteps are inevitable, recognizing common debt pitfalls puts you on guard to avoid or address them rapidly. Monitor your spending, increase savings, thoroughly research financial agreements, and prioritize education.

These small steps create the foundation for a lifetime of financial security and freedom from debt. The time is now to stop digging. With prudence and discipline, you can steadily fill that hole back in.

Debt can feel overwhelming, but the key is addressing issues early before they spiral. By learning from common financial mistakes, you gain awareness to avoid future pitfalls. While missteps are inevitable, equipping yourself with financial literacy, budgeting diligently, establishing emergency savings, and planning puts you on solid ground.

Don’t let anxiety about debt paralyze you; instead, cultivate financial resilience. With a little effort each day, you can steadily pay down balances, increase savings, and build solid financial habits that lead to long-term security.

The journey begins with knowledge, discipline, and an empowered mindset to take control. You can overcome debt and forge a stable financial future. Begin by making small, consistent changes—your future self will thank you.

The debt snowball and avalanche methods are proven strategies, so pick the one that best fits your personality. Avalanche tackles the highest interest rate debts first to save on total interest paid, while Snowball targets the smallest balance debts first to stay motivated by quick wins.

Read personal finance books, take community college courses, listen to financial podcasts, and meet with an unbiased monetary advisor to better understand budgeting, taxes, investing, insurance, and planning for retirement and other goals. Having a solid financial education empowers you to make wise decisions.

It’s always possible to start saving! Even if you are creating late compound interest, contributing what you can increases your earnings over time. Take full advantage of tax-advantaged retirement accounts like 401(k)s and IRAs and use retirement calculators to determine target savings amounts to reach your goals.