Quick Decision Framework

- Who This Is For: Ecommerce founders, DTC operators, and Shopify merchants who want to understand how OpenAI’s capital structure and IPO trajectory will shape the AI tools, infrastructure pricing, and platform stability they depend on to run their businesses.

- Skip If: You have no interest in the financial mechanics behind AI infrastructure and only want tactical platform or app recommendations.

- Key Benefit: Understand the specific concentration risks, debt dependencies, and capital allocation shifts inside OpenAI’s $852 billion valuation so you can make more informed decisions about which AI tools and partnerships to build your stack around.

- What You’ll Need: No prior finance background required. Familiarity with OpenAI, Microsoft Azure, and SoftBank as names is sufficient context to follow the analysis.

- Time to Complete: 6 minutes to read. No immediate action required; this is orientation and awareness content.

The companies building on top of AI infrastructure are not insulated from the financial risks inside it. Understanding who holds the debt matters as much as understanding who holds the data.

What You’ll Learn

- Why OpenAI’s $852 billion valuation carries structural concentration risks that go beyond typical pre-IPO volatility.

- How the financing relationships between OpenAI, Microsoft, SoftBank, Amazon, and Nvidia create a closed-loop capital dependency that limits strategic flexibility.

- What the shift from expansive growth to selective resource allocation signals about OpenAI’s path toward long-term profitability.

- How SoftBank’s debt exposure and declining stock price are beginning to transfer OpenAI’s financial risk to the broader investor market.

- Why investors evaluating a potential OpenAI IPO are moving from growth optimism to a more measured assessment of infrastructure diversification and capital sustainability.

The rapid growth of OpenAI’s valuation in the private capital market is bringing the company closer to a projected IPO with a capitalization of over $1 trillion. However, the structure of this growth is becoming a key source of risk. The latest financing round — in which the project raised $122 billion, exceeding the planned $110 billion target — brought the valuation to $852 billion. At the same time, a significant part of these funds is provided by a select group of strategic investors such as SoftBank, Amazon, and Nvidia, increasing capital concentration and creating a closed-loop financing effect within the AI ecosystem.

Despite monthly revenue growth to about $2 billion, OpenAI remains in an aggressive investment phase where capital expenditures significantly outpace current inflows. This is prompting a reassessment of priorities: the company is abandoning less profitable areas and taking a more cautious approach to building its own infrastructure, transferring some of the projects to partners. This shift reflects a transition from an expansive growth model to a more selective allocation of resources, which is an important signal for investors ahead of a potential OpenAI IPO.

Dependence on external financing and infrastructure remains a primary risk factor. In recent investor disclosures, OpenAI explicitly highlighted its dependence on Microsoft, which has not only invested at least $13 billion in the startup but also provides access to computing power through Azure. This concentration of resources from one partner limits strategic flexibility and may trigger market skepticism during IPO preparation. Additional pressure comes from the company’s dependence on hardware vendors, including semiconductor manufacturers, as well as the need to invest up to $665 billion in infrastructure by 2030.

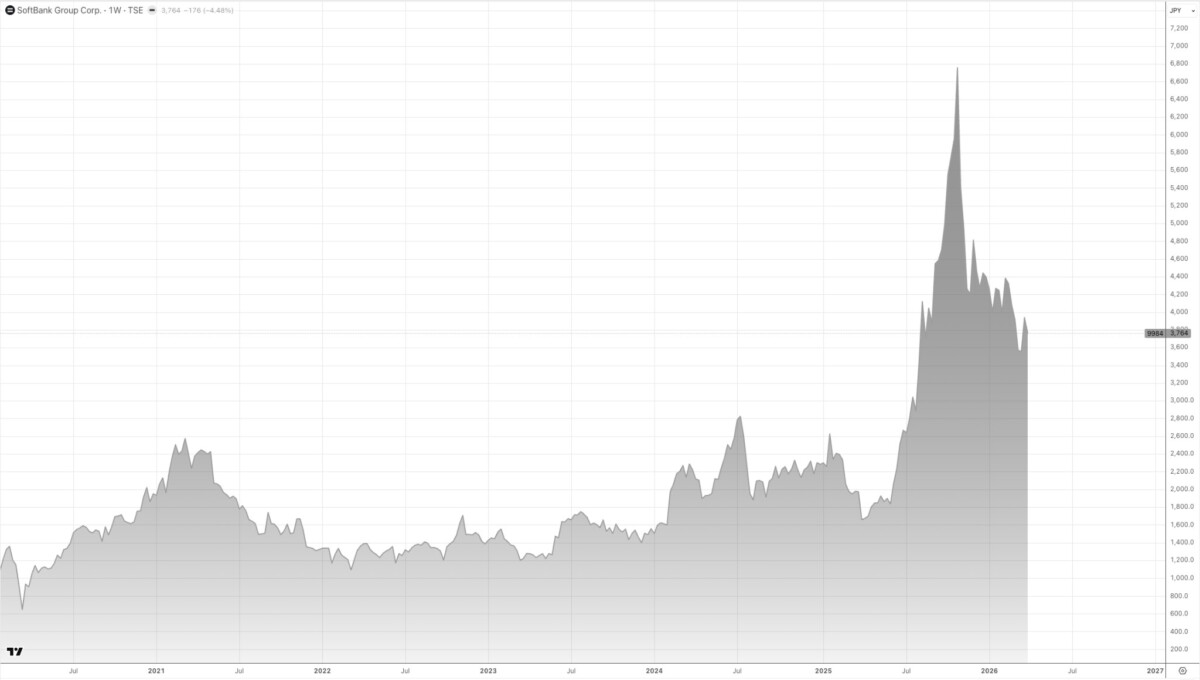

The financial burden also extends to key investors. SoftBank — having committed roughly $34 billion to OpenAI, funded in part by a massive liquidation of its Nvidia stock — is now preparing to raise up to $30 billion in borrowed funds, potentially pushing its debt above historical levels. A growing share of non-public assets and recent credit rating concerns reflect market doubt regarding the payback period for AI infrastructure. The 45% decline in SoftBank’s stock price since October 2025 demonstrates that risks associated with OpenAI are beginning to spill over to investors, increasing the project’s systemic importance for financial markets.

In response, OpenAI is attempting to diversify its capital sources and reduce dependence on a single partner by expanding cooperation with alternative cloud providers and attracting a wider range of investors. However, this strategy complicates the company’s financial structure. Venture capital, debt financing, and infrastructure contracts are becoming increasingly intertwined, forming a multi-layered model that is sensitive to shifting market conditions.

Thus, OpenAI remains the primary driver of the AI sector, demonstrating an unprecedented ability to scale revenue and attract capital. Yet, the mounting risks associated with partner dependence, investor debt, and massive capital requirements cannot be ignored. In this environment, investors are becoming more selective, shifting from optimism to a more nuanced assessment and considering not only growth, but also the stability of the financial model, infrastructure diversification, and the company’s ability to convert large-scale investments into long-term profitability.

Frequently Asked Questions

What is OpenAI’s current valuation and how was it reached?

OpenAI’s current private market valuation is $852 billion, reached after a financing round that raised $122 billion, exceeding the company’s own $110 billion target. The valuation reflects investor confidence in OpenAI’s revenue trajectory and market position, but also incorporates the concentrated capital structure and infrastructure dependencies that represent the primary risk factors heading into a projected IPO above $1 trillion.

Why is OpenAI’s dependence on Microsoft considered a risk factor?

OpenAI’s dependence on Microsoft is a risk factor because Microsoft is simultaneously one of OpenAI’s largest investors (at least $13 billion committed) and its primary infrastructure provider through Azure. This dual relationship limits OpenAI’s ability to negotiate infrastructure pricing, pursue alternative cloud partnerships, or make strategic pivots without affecting a relationship that is both financially and operationally critical. OpenAI has disclosed this dependence explicitly in investor materials as a primary risk.

How does SoftBank’s financial situation affect the OpenAI IPO outlook?

SoftBank has committed roughly $34 billion to OpenAI, funded in part through Nvidia stock liquidations, and is now preparing to raise up to $30 billion in additional borrowed funds to sustain its position. SoftBank’s stock price has declined approximately 45% since October 2025, reflecting market concern about AI infrastructure payback timelines. This creates a risk transfer effect: stress at the anchor investor level can reduce market confidence in the IPO story and widen the gap between private market valuation and public market pricing.

What does OpenAI’s $665 billion infrastructure investment target mean for profitability?

OpenAI’s estimated infrastructure investment requirement of up to $665 billion through 2030 means the company will remain in a capital-intensive growth phase for the foreseeable future, even as monthly revenue approaches $2 billion. The gap between current inflows and required capital expenditure is the primary reason OpenAI continues to depend on external financing and why the company is shifting toward more selective resource allocation, prioritizing high-return areas and transferring some infrastructure development to partners.

How should ecommerce businesses think about OpenAI’s financial risk when building AI-powered workflows?

Ecommerce businesses building on OpenAI-powered tools should treat the company’s capital structure as a platform stability signal. Concentration of infrastructure in Microsoft Azure, dependence on a small group of strategic investors, and the scale of ongoing capital requirements mean that pricing, availability, and product direction for OpenAI tools are all subject to financial pressures that are not visible in the product interface. Building workflows that are portable across AI providers, rather than deeply locked into a single model or API, reduces exposure to the downstream effects of OpenAI’s capital decisions.