The DHL and USPS last-mile deal signals the US last mile is consolidating around a Postal Service that has stopped undercharging for it. Shopify merchants should expect last-mile rates to keep climbing and treat their fulfillment model, not their carrier label, as the real lever on shipping cost.

Everyone read this deal as a sign the Postal Service is in trouble. It is the clearest sign yet that USPS has figured out how to charge what its network is worth.

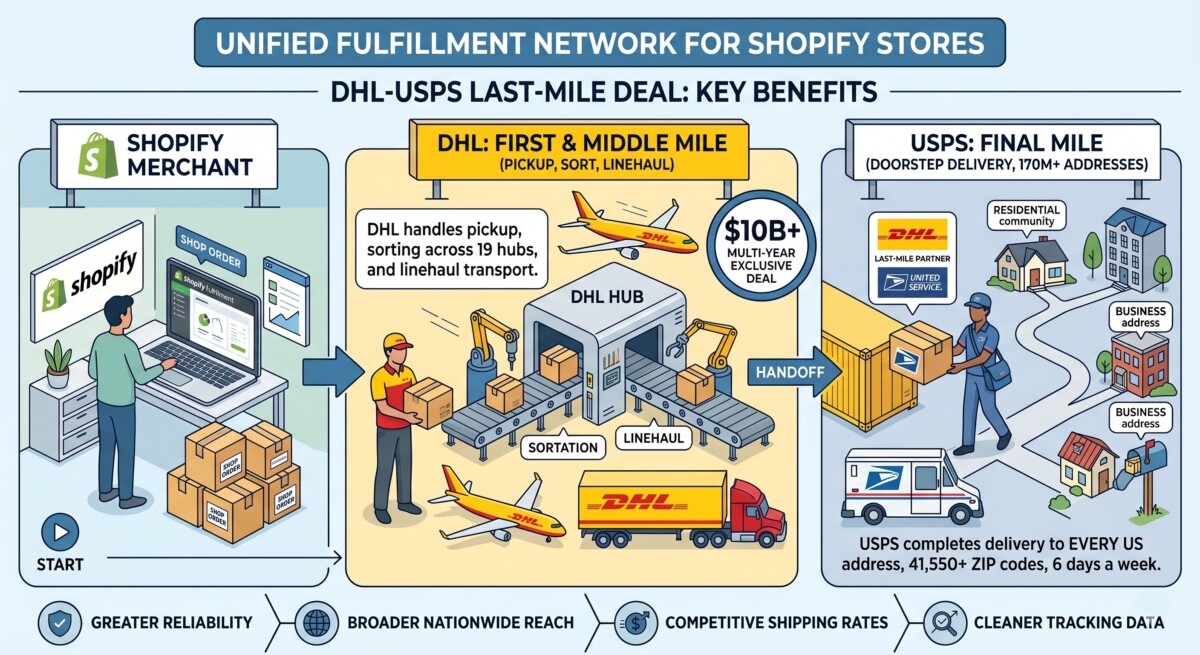

On May 28, 2026, DHL eCommerce signed an exclusive multi-year contract handing the United States Postal Service the entire final mile for its US parcels, a deal valued at well over $10 billion. It moved through most of the weekly roundups as a single line, filed under the usual USPS-is-struggling narrative.

That framing misses what happened. The last mile, the most expensive leg of any shipment, is consolidating around USPS as commercial shared infrastructure, and the Postal Service has stopped pricing that infrastructure like a charity. If you are a Shopify operator doing $500K to $5M and you own your shipping costs, this is the signal worth reading, because it tells you where your fulfillment economics are heading over the next several years.

One honesty note up front. This is not a feature you switch on. DHL is outsourcing its own last mile here, not handing you a new button in Shopify Shipping. The value is in what the move signals about your options and your costs, and in the fulfillment decision it should prompt you to revisit.

DHL eCommerce handed USPS the entire final mile for its US parcels in an exclusive, multi-year contract worth well over $10 billion, and the larger story is USPS opening its residential network as shared infrastructure that any large shipper can now buy into. This is the largest agreement in the 25 year DHL eCommerce and USPS relationship, and the first to lock in this much volume for this long.

DHL keeps the parts of the chain it is good at and rents the part that is hardest to build. DHL eCommerce handles nationwide pickup, sortation across its 19 fully automated US hubs, and linehaul on its air and ground network. USPS performs the final-mile delivery into more than 41,550 ZIP codes and more than 170 million delivery points, six days a week. No private carrier can replicate that residential density, which is exactly why DHL is paying to use it rather than build it.

The deal is the third domino in a pattern that has been building all year. USPS opened its last-mile network to competitive bidding in January 2026, inviting large and small shippers to buy access it once reserved for a few giants. In April 2026, Amazon settled what had been a threatened two-thirds pullback into a roughly 20% volume cut, leaving USPS handling about 80% of Amazon’s parcels, more than a billion packages a year and an estimated $6 billion in annual revenue. DHL locking in an exclusive long-term contract is the clearest confirmation yet that USPS is becoming the shared residential backbone other carriers plug into, on USPS terms.

USPS is not about to disappear; it is a government-mandated universal carrier repositioning to earn real revenue, so the risk to your business is pricing and service levels, not collapse. The Postal Service posted a $9.0 billion net loss for fiscal year 2025, an improvement on the $9.5 billion loss the prior year, with cumulative losses of roughly $118 billion since 2007. Postmaster General David Steiner has warned about the cash imbalance, but his stated fix is to raise revenue and compete harder, and revenue did grow last year on the back of Ground Advantage and price increases.

A government-backed universal carrier does not behave like a normal company facing those numbers. Look north for the proof. Canada Post has run heavy losses, weathered repeated strikes, and gone through restructuring after restructuring, yet it persists because the universal service obligation outlives any single year’s balance sheet. The mandate to reach every address is a political commitment, not a quarterly earnings call. USPS sits in the same category. Betting your fulfillment plan on it vanishing is planning for a risk that the structure of the institution is designed to prevent.

What changes is price and service, not existence. A carrier that has spent years undercharging for its last mile, while losing $9 billion a year, has every incentive to keep raising rates and to adjust service levels where the economics demand it. For a Shopify merchant, that means your USPS line item climbs and your delivery standards may shift, and you should budget and plan around exactly that. The Postal Service is not going away. It is getting more expensive and more commercially run, which is a very different problem to manage.

Expect last-mile rates to keep climbing, because USPS has already raised shipping prices twice in 2026 and is rerating large, lightweight parcels in a way that quietly raises the cost of common ecommerce shipments. The era of USPS as the reliably cheapest option is closing, and the changes are stacking faster than most operators have noticed.

Three pricing actions hit in a single year. On January 18, 2026, USPS raised competitive shipping prices, with Ground Advantage up about 7.8%, Priority Mail about 6.6%, Priority Mail Express about 5.1%, and Parcel Select about 6.0%. Then, in a move that surprised the industry, USPS layered a temporary 8% surcharge on those same four competitive services, in effect from April 26, 2026 through January 17, 2027, functionally a fuel surcharge by another name. A third action followed on July 12, with mailing services rising about 4.8% and the First-Class Forever stamp going from 78 to 82 cents. Stacked together, a typical lightweight DTC parcel can run roughly 15 to 20% more than it did in late 2025.

The change with the biggest hidden cost is the dimensional weight divisor dropping from 166 to 139, effective July 12, 2026, which brings USPS in line with how UPS and FedEx already bill. Billable weight is your package’s cubic size divided by that divisor, so a smaller number means a higher billed weight. A box measuring 12 by 12 by 12 inches bills at about 10.4 pounds under the old 166 divisor and about 12.4 pounds under 139, roughly 19% more, even though nothing inside the box changed. If you ship pillows, apparel in oversized mailers, or any light, boxy product, your cost just went up without a single rate-card line moving. USPS also added a $3.00 fee for parcels with missing or incorrect dimensions, so sloppy package data now carries its own penalty.

The question this deal raises is not whether to switch carriers; it is whether your fulfillment model still fits a more expensive, more consolidated last mile. There are three honest models, and the right one depends on your volume and stage, not on which one a vendor is selling you. This is the cost and model side of shipping; the customer-facing side, the promise you make at checkout, is its own decision covered in rebuilding your free shipping promise for 2026.

Self-fulfillment still wins when control matters more than rate leverage and your volume is modest. Shipping from your own garage or warehouse means no 3PL margin sits between you and the carrier, and you keep full command of packaging, inserts, and the unboxing experience. The catch is that you pay near-retail or only lightly discounted USPS rates, and you absorb every one of the 2026 increases directly, with no provider’s negotiated rate card to cushion you. For a Starting brand at $50K to $500K shipping a few hundred orders a month, that tradeoff often still favors keeping it in-house.

A 3PL or consolidator wins when the scale you can borrow beats the control you can keep. A 3PL gives you negotiated carrier rates, zone coverage from multiple warehouses, and the ability to ride a provider’s volume, in exchange for per-order fees and less hands-on control. A consolidator is what DHL eCommerce itself is: it aggregates parcels from many shippers to inject them deep into the USPS network at rates no single brand could command, which is precisely the economics this deal scales. As your order count climbs into the thousands per month, those models usually come out ahead. Use the comparison above and read the practical detail in this guide to getting the most from a 3PL partnership, including the hybrid setups many Scaling brands settle on.

Ask the questions that expose how exposed you are to the 2026 rate path. What carriers and consolidator relationships do you have access to, and how are the temporary 8% surcharge and the new DIM divisor reflected in my quoted rates? What is my true blended cost per order under each model once storage and per-order fees are included? Where do my customers actually live, and how much of my volume hits surcharged rural or remote zones? If you are weighing a switch, the framework for choosing the right 3PL for your stage will keep the decision grounded in your numbers rather than the sales pitch.

The deal is mostly good news: a stronger DHL plus USPS combination is a more credible alternative to the UPS and FedEx duopoly, and more volume funding the USPS network helps preserve the six-day rural reach many brands quietly depend on. It is worth holding this alongside the rate pressure, not in place of it, but the structural picture has real benefits.

A better-funded DHL and USPS pairing puts more competitive pressure on the two carriers that have set the pricing tone for a decade. UPS spent 2025 reorienting around profit over volume, lifting revenue per piece by about 8.3%, and both UPS and FedEx layer on accessorial fees most operators have learned to dread. A third credible national option with genuine residential density gives merchants negotiating leverage they have lacked, and competition at the carrier level tends to help merchant rates at the margin over time.

The volume flowing into USPS helps fund the one thing no competitor wants to build: affordable, six-day delivery to every rural address. The last mile already accounts for up to 53% of a shipment’s total cost, and private carriers price that reality bluntly. In 2026, UPS lists a remote-area surcharge of $16.50 and FedEx a remote delivery surcharge of $16.75 on certain ZIP codes. If a meaningful share of your customers live outside dense metros, a financially healthier USPS network is what keeps those orders economical to serve, for you and for them.

What to do depends on your stage, but every operator should at minimum reprice their shipping assumptions for a last mile that keeps getting more expensive. The deal itself requires no action; the cost environment it confirms requires plenty. If you are Starting at $50K to $500K, you are likely on USPS through Shopify Shipping already, so your move is to understand the rate path and the DIM divisor change rather than switch anything, and to set realistic free shipping thresholds against the new costs. If you are Scaling at $500K to $2M, run the carrier-mix and 3PL decision in earnest and model the new DIM divisor against your actual package profile before you renew anything. If you are Established at $2M and above, use your volume as negotiating leverage, evaluate a multi-carrier and zone strategy, and treat last-mile cost as a managed line item rather than a pass-through you discover at month end. A practical first move at any stage is to pull your blended shipping cost per order from the last 90 days, layer on the stacked 2026 increases, and check whether your free shipping threshold still protects your margin. Plenty of brands find an old threshold set in 2024 now quietly loses money on every order that just barely qualifies. Whatever your stage, this is the moment to build a shipping strategy that matches what you sell and who buys it instead of inheriting one by default.

The DHL and USPS last-mile deal is an exclusive, multi-year contract valued at well over $10 billion, in which DHL eCommerce hands USPS the final-mile delivery of all its US parcels while keeping pickup, sorting across its 19 automated hubs, and linehaul. It does not give your Shopify store a new button to switch on, because DHL is outsourcing its own delivery here. What it affects is the direction of last-mile economics. It confirms USPS is positioning its residential network as shared infrastructure that large shippers buy into, and that the Postal Service intends to be paid market value for it. For merchants, the takeaway is about where shipping costs and fulfillment options are heading, not an immediate feature change.

Yes, USPS shipping rates are very likely to keep rising through 2026 and beyond. USPS raised competitive shipping prices on January 18, 2026, lifting Ground Advantage by about 7.8% and Priority Mail by about 6.6%, then added a temporary 8% surcharge on Priority Mail, Priority Mail Express, Ground Advantage, and Parcel Select that runs from April 26, 2026 through January 17, 2027. A mailing services increase followed on July 12. Stacked together, a typical lightweight ecommerce parcel can cost roughly 15 to 20% more than it did in late 2025. The Postal Service has openly said it must raise revenue, so plan your 2026 and 2027 shipping budgets around continued increases rather than a return to flat pricing.

No, USPS is not going out of business. It posted a $9.0 billion net loss in fiscal year 2025 and its leadership has warned about cash pressure, but USPS is a government-mandated universal carrier obligated to deliver to more than 170 million addresses six days a week. Its strategy is to raise revenue and change pricing, not to shut down. The more useful way to plan is to treat USPS the way you would any carrier that has decided to charge what its network is worth: assume higher rates and evolving service levels, not disappearance. Building your fulfillment plan around USPS vanishing would be planning for the wrong risk entirely.

It depends on your order volume and stage, not on the headlines. If you ship a few hundred orders a month and value control, self-fulfillment can still win, since you avoid per-order 3PL fees, though you pay near-retail rates and absorb every increase directly. Once you are consistently shipping thousands of orders a month, a 3PL’s negotiated rates, zone coverage, and borrowed scale usually outweigh the per-order fees and the loss of hands-on control. Many Scaling brands land on a hybrid: keep high-touch or high-value SKUs in-house and push the rest to a 3PL. The right move is to run the math on your blended cost per order under each model rather than defaulting to whatever you do today.

The USPS dimensional weight change lowers the DIM divisor from 166 to 139 as of July 12, 2026, which raises the billable weight of large but lightweight parcels. Billable weight is calculated by dividing a package’s cubic size by the divisor, so a smaller divisor produces a higher number. A box measuring 12 by 12 by 12 inches bills at about 10.4 pounds under the old 166 divisor and about 12.4 pounds under 139, roughly 19% more, even though nothing inside the box changed. If you ship pillows, apparel in big mailers, or other light, boxy products, expect higher costs and review your packaging dimensions. USPS also added a $3.00 fee for parcels with missing or incorrect dimensions.