Improving cash flow is a smart move for any business. It doesn’t matter how great your business model is, how profitable you are, or how many investors you have lined up. If you’re looking for one area to focus on that will have a dramatic impact on your business, this is it.

New and growing businesses often don’t have a buffer of extra cash to get them through shortfalls, because they are always reinvesting. Years with the most significant growth—including the first few years of a business’s lifespan—are also challenging when it comes to cash flow.

Cash flow management is one of many reasons it’s so hard to get a new business off the ground.

So, what is cash flow management exactly? Cash flow is the amount of money, cash and non-cash, traveling into and out of a business. A positive cash flow is more money coming in than going out, and a negative cash flow is less money coming in than the business needs to cover outgoings.

To calculate cash flow, a business takes note of the cash available at the beginning and at the end of a specific period. This time period may be a week or a month. The business will have a positive cash flow if there is more in the account at the end of the period than when the period began; it will have a negative cash flow if there is less cash at the end.

Getting good at cash flow management is one of the best things you can do for your business. Not only that, it’s a skill you can carry over into other ventures, as well as your personal finances.

Forecast your cash flow with confidence

We’ve put together a cash flow forecast template to help streamline the process and save you time and stress. Download and read on to learn how to use it.

Cash flow is not the same as profitability. A profitable business can still be unable to pay its bills. Similarly, just because a business is meeting all of its financial obligations doesn’t mean it’s profitable.

Profit is a basic small business accounting term, which really only exists on paper. Measuring profit is a particular way of looking at a business. It doesn’t tell you a whole lot about how the business is getting by day-to-day.

The first step to calculating profit is to take your total revenue and then subtract the cost of goods sold. The difference is your gross profit.

Revenue – Cost of Goods Sold = Gross Profit

For example, if you sold $100,000 in rocking chairs and the chairs themselves cost you $50,000 wholesale, your gross profit would be $50,000.

Revenue: $100,000

Cost of Goods Sold -$50,000

Gross Profit: $50,000

Of course, you would probably have other expenses beyond buying the chairs. For example, you’d need a place to store the chairs, and you might want to run some ads to get more sales. These expenses are called operating expenses, and they get subtracted from your gross profit.

Operating expenses include most costs that don’t directly connect to what you sell—things like rent, equipment, payroll, and marketing.

The second step is to subtract operating expenses from gross profit. The difference is net profit.

Gross Profit – Operating Expenses = Net Profit

Revenue: $100,000

Cost of Goods Sold: -$50,000

Gross Profit: $50,000

Operating Expenses: -$35,000

Net Profit: $15,000

If your net profit is a positive number, you made money. If it’s a negative number, you lost money. This report as a whole is called the income statement, or profit and loss (P&L).

In relation to small business cash flow management, the problem with income statements is that they don’t show your whole business. A few essential pieces of information are missing.

If you have any business loans or other startup capital to repay, it won’t show up here. Only the interest on those loans is included on a P&L, even though debt repayments can eat up a lot of cash.

Similarly, if you make a significant equipment purchase, the entire cost will not show up in this section. Instead, that cost will get spread out over the lifetime of the equipment. If you spend $100,000 on a canning line and you think it will last you 10 years, your income statement will show an expense of $10,000/year for 10 years, even if you had to pay all of it upfront.

Note that your net profit isn’t taxed at this point, which means it will shrink even more. Even if all of your profit is available in cash, you won’t be able to run out and spend it all in one place.

Finally, many businesses use accrual accounting, which records revenue even if you haven’t received the money yet. On paper, you might have $200,000 in sales, but if no one has paid you yet, you’re still going to have a hard time paying your bills.

Further, if you carry inventory, all that product has value and gets included on your income statement as well. Of course, to extract cash from your inventory, you need to sell it first.

Ultimately, managing cash flow comes down to timing. You may be profitable over the course of a month or a year, but not over a specific day or week. If your bills are due at the beginning of the month but you won’t have any money in the bank until the end of the month, you’ve got a cash flow problem, even if at the end of the month you made more than you spent.

Here’s the deal with profit: if you’re not profitable on paper, you’re in bad shape. You need to either increase your revenue or decrease your expenses if you want to stay in business.

But just because you’re profitable doesn’t mean your business can run on autopilot. You still need to practice cash flow control—especially if you’re growing.

Although it may seem intimidating, there are clear benefits to cash flow control and prioritizing effective cash flow management.

The first and most obvious benefit to managing cash flow and working capital is knowing ahead of time when you’re going to have shortfalls. Don’t find out you can’t make rent after the check bounces. With a good system in place, you can predict shortfalls weeks, sometimes even months, ahead of time, which gives you time to come up with a plan.

For example:

Believe it or not, managing cash flow will alleviate a lot of stress. Much of the anxiety entrepreneurs experience around paying bills comes from not knowing what’s going on and worrying about whether or not things will work out.

It’s much better to know what’s coming, even if the outlook is not good. When you know where you stand, you’ll feel prepared. More importantly, you’ll be equipped to deal with it.

When you’re managing cash flow, you know exactly how much money you have to spend on growth. Remember, just because your P&L tells you there’s extra money lying around, doesn’t mean it will materialize in real life.

Similarly, just because you have $20,000 in the bank doesn’t mean you can spend it. You might need it to pay for upcoming expenses. When you look at your cash flow over weeks and months, you’ll know how much to keep on hand and how much you can stash away or spend on growth.

Good cash flow management gives you leverage. If you need a line of credit from the bank to get you through a shortfall or you want to get a supplier to give you a break for a few weeks without interrupting service, a good cash flow management system will back you up and establish trust.

Banks generally like to see this kind of planning, especially if you can clearly show when you’ll be able to repay the funds. Suppliers are much more likely to be flexible if you can tell them exactly how you’ll pay and when—rather than cutting communication like most businesses do during tough periods. These people want your business and will be more willing to work with you through the ups and downs if they can trust you.

Cash flow is significantly more accurate than a budget. Budgets tell you what you want to happen. They’re wishful thinking, and entrepreneurs are optimistic by nature. Cash flow projections tell you what is actually happening so you can deal with it—even if it’s not what you planned at the beginning of the year.

Most of us (myself included) would often rather not think about managing cash flow and just hope it all works out. But it’s not worth the risk. You really will feel better by staying on top of your money.

There are many paid tools out there to help manage cash flow. Personally, I think the free one is the best one: Google Sheets. Anyone can use a Google spreadsheet to create a cash flow statement. Although it’s a manual process, it doesn’t take long to set up, and it’s easy to track.

More importantly, it’s easy to customize on the fly and adapt to your specific needs or situation. You can be as broad or as specific as you want. And the time you spend creating and updating your spreadsheet is valuable for gaining a clearer picture of your situation.

The cash flow spreadsheet is an outline of where your cash is going. It shows you when cash will be coming in, and when it will be going out, and it’s a great way to visualize cash flow management and adjust your approach.

The best way to keep control of your money is with a cash flow statement. In small business cash management, a cash flow statement is an account of the cash flowing into and out of a business over an accounting period, such as a month, quarter, or year, although you can track cash flow for any time period that helps you see where your money is going.

Most businesses work best by planning week to week; however, some may need to plan daily, others only need to plan monthly. It’s also up to you if you want to include every single expense or just categories of expenses. These decisions will depend on the scale and complexity of your business.

Similarly, some businesses will be able to project their cash flow accurately for six months, others only two weeks. In general, try to project four to six weeks with reasonable accuracy. A good rule of thumb for small business cash flow management is that the farther you are into the future, the less accurate your predictions will be.

The first step is to lay out all of your ongoing financial obligations. Start by making a list of everything you have to pay for—rent, salary, advertisements, software fees, loan repayments—anything that comes out of your bottom line.

Write down what the expense is for, how much it is, and when it’s due. You’ll likely forget a few things, so review your bank and credit card statements to see what other expenses you find.

Next, it’s time to forecast your weekly revenue. Many businesses experience fluctuations in sales, so it can be a bit of an art. Try to be as accurate as possible. The more established your business becomes, the easier it will be.

Start by writing down any guaranteed revenue. If you sell subscriptions or have long-term contracts, you’ll have a good idea of what’s coming up. You can estimate if those numbers are going to go up, down, or stay the same. If a large portion of your sales come from first-time customers, it will be more difficult to estimate. Still, you should have a good idea of what to expect over the coming weeks and months. The closer you can get to reality, the better.

One best practice in small business cash management is looking at past data to assist projections. In many cases, your sales from this week one year ago will be more accurate than your sales last week, because historical data takes annual cycles and seasonality into account. If you believe your sales will grow over last year’s, you can increase the amount, but it’s important to be conservative to avoid ending up in a bad situation.

As you forecast revenue each week, be mindful of any dips in sales due to holidays or the time of month or year, as well as any promotions or major deals that will positively impact your revenue.

Now comes the fun part—filling in your data. First, grab your free copy of the cash flow projection template. You can customize a row for each expense and each revenue source. You can be as detailed or as broad you need to be.

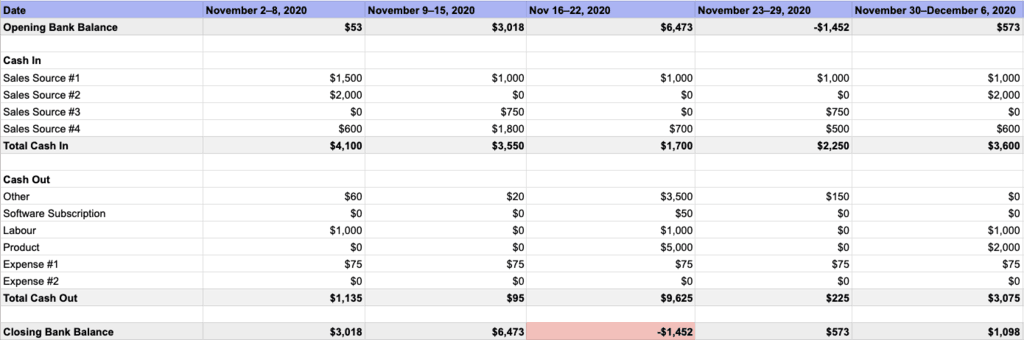

Take a look at this business cash flow management example below.

If you sell a bunch of products on one website, you may only have one source of revenue. If you use multiple channels, such as web, retail, and trade shows, you might want to have a line for each, because it will be easier to predict.

Make sure you add revenue to the week it will become available to you. Keep in mind that it may take a few days to end up in your bank account.

Similarly, fill in your expenses. Some will be weekly, some bi-weekly, some monthly, some variable. You’re also going to have a lot of miscellaneous expenses popping up. Use the row labeled “Other” to work these into the spreadsheet.

Add your opening bank balance for the first week. The following weeks will be predicted automatically based on your revenue and expense projections.

Your cash flow spreadsheet is a living document. If you keep it as a Google Sheet, it will be available anytime, anywhere. You’ll also be able to easily share it with someone else, such as your accountant or another employee.

A good cash flow spreadsheet is updated on a regular basis. Once a week, log in and update your closing bank balance. If it doesn’t match your previous calculations, it’s a good idea to figure out why. Sometimes expenses you forgot about pop up, or you realize you may have been too optimistic in your revenue projections.

Next, hide last week’s column. You won’t need it anymore since it’s in the past.

Finally, add a new week of projections in the last column. You always want to have a minimum of four to six weeks laid out so you can plan ahead.

Any time you’re projecting a shortfall, the closing bank balance will alert you by turning red, which prompts you to make some changes. In the template provided, you can see that a shortfall is predicted in the third week.

According to this cash flow management example, the company could contact their product supplier and renegotiate their next payment. Instead of paying all $5,000 that week, they could ask to pay $3,000 and settle the remaining $2,000 the following week.

If your business is suffering from poor cash management, here are seven ways to improve cash flow today.

With cash flow management in mind, consider updating inventory to reflect current supply-and-demand levels in your business. Do frequent inventory checks to determine what’s selling and what’s not. Then, you can keep more inventory on hand that’s likely to move fast and get rid of dead stock at a discount.

Small business finance is always tricky, especially during challenging times. You don’t want to get into much debt, but sometimes you need to invest in equipment or inventory that’ll pay off in the long run. Good cash management practices would be to lease rather than buy. When you lease, you can make small payments over time and keep cash flow for your day-to-day operations. It’s also a business expense, so you can write it off on your taxes.

One key part of small business cash flow management is getting paid as soon as possible. If you send out invoices immediately, receivables will come in faster. If you typically operate on a monthly billing cycle, talk with your vendors to let them know you’ll be moving to an invoice-on-demand model. Bonus points if you offer them an early pay discount.

If your scenario is changing and putting pressure on your current revenue streams, look for alternative ways to make money. You may be able to temporarily, or even permanently, replace less profitable revenue streams with easier, more effective ones.

For example, the COVID-19 spread has shuttered many bricks-and-mortar businesses due to mandatory shutdowns. A main source of cash flow for these businesses is foot traffic. To combat the drop in revenue, they are moving their business online and offering different shopping experiences, like “Buy Online, Pickup Curbside” and local delivery options.

This can help make managing your cash flow easier and take pressure off your top line.

One way to preserve working capital and cash flow management is to pay suppliers less. Some suppliers may have early pay discounts you aren’t aware of. Paying your suppliers early can help you save cash and even improve the integrity of your supply relationships, especially if other vendors are delaying payments in abnormal business conditions.

To maximize your cash flow, put money into a high-interest business savings account. Find an account that gives you more than 1% for leaving your cash in it, with a low minimum deposit. This can improve your cash position month by month and help you prepare for any unforeseen impacts on your customers or suppliers.

If you have poor cash flow, consider raising the price of your products. Start by asking yourself:

Look for opportunities to keep your prices competitive but also make a profit. If you price too low, your company may come off as cheap. If too high, you might scare potential customers off.

Positive cash flow in financial management shows that a business’s liquid assets are increasing. With a positive cash flow, you can settle debts, reinvest in your business, pay expenses, and create a hedge for financial challenges in the future. In business financing, a company with strong cash flow can take advantage of lower interest loans and more profitable investments.

To start a cash flow, you’ll need to sell more than you are spending. You can predict cash flow by preparing a forecast:

In small business cash flow management, the main objective of managing cash flow is to track and analyze the amount of cash received minus business expenses. This helps estimate what you’ll make and spend in the future and maintain your business during emergencies.

Cash flow is important in cost management because it helps plan and control the budget of a business. An accountant can better forecast if you can make payment for assets that help your business run, such as raw materials, stock, employees, rent, and other related expenses.

Most companies cannot survive without proper cash flow management. But anyone can do it. Take the time to get organized now, and it’ll be easy to stay on top of it.

If you haven’t already, don’t forget to grab your free cash flow template. You can access the spreadsheet in Google Drive. You’ll need to be logged into your Google account to make a copy.

How do you track your cash? We’d love to hear about it in the comments!

Illustration by Till Lauer

This article originally appeared in the Shopify blog and has been published here with permission.