Every regulated money movement license Shopify earns is one more reason your store will not move when you eventually want it to. That is not necessarily a problem. It is a decision to make deliberately, before the cost of the decision compounds for you.

On Tuesday, Shopify reported Q1 2026 GMV of $101 billion, with Merchant Solutions revenue (the financial services side of the business) growing 39 percent to $2.42 billion. That number is now roughly three out of every four dollars Shopify earns. Five days earlier, The Information reported that Shopify is quietly pursuing money transmitter licenses in every U.S. state. The two stories are the same story.

For most coverage, the licensing news landed as a one-line headline. For most merchants, it landed without explanation. But for any operator running a Shopify store between $500K and $10M in revenue, this is the most important strategic shift on the platform since Shop Pay launched in 2017. It is going to change your costs, your options, and your dependence on Shopify in ways that compound silently over the next 18 to 24 months.

Here is what is actually happening, why it matters for your margins, and the independence trade-off every founder and operator should think through before the back half of 2026.

Shopify is pursuing money transmitter licenses in every U.S. state and territory, currently holds approvals in 18 states plus Puerto Rico, and has applications under regulatory review in California, New York, and the remaining jurisdictions, according to trade press coverage of The Information’s reporting on Shopify’s regulatory filings.

A money transmitter license is a state-level authorization that allows a company to hold and transfer money on behalf of others. In addition to the money transmitter designation, Shopify has told regulators it intends to operate as a “provider of prepaid access,” which is the regulatory category that enables wallet-style functionality where consumers and businesses can store funds in an account, similar to how Venmo, Cash App, and PayPal hold customer balances today.

Right now, Shopify Payments is operationally Shopify’s product, but the regulated parties underneath it are Stripe Payments Company (the licensed money transmitter), Fifth Third Bank (where merchant funds are held), Celtic Bank (issuer of the Shopify Balance and Shopify Credit Visa cards), and WebBank (originator of Shopify Capital loans). Shopify orchestrates the merchant experience. The regulated entities are partners.

The hiring patterns make the project’s seriousness visible. Recent job postings reference a “money movement platform,” include positions requiring BIN sponsorship experience (the regulated banking arrangement that lets a non-bank issue payment cards), and even a Luxembourg-based role suggesting cross-border money movement infrastructure is also in scope.

Ken Wong, managing director at Oppenheimer, told The Information that fuller licensing could let Shopify offer new merchant capabilities, such as automated invoicing, and “increase the take rate” and “the margins on a per-merchant basis.” That is the financial frame. Shopify becoming a regulated money transmitter unlocks new revenue and reduces the partner economics it currently shares with Stripe and others on every dollar that moves.

Shopify’s Q1 2026 earnings tell you why the money transmitter push exists: Merchant Solutions revenue (the take-rate-driven side of the business) grew 39 percent to $2.42 billion in a single quarter, accounting for roughly three out of every four dollars Shopify earns, according to the official quarterly results disclosure.

The numbers underneath that headline matter more. Shopify Payments processed $67 billion in GMV during Q1, which is 41 percent higher than the prior year and represents 67 percent of total GMV (up three percentage points year over year). Shop Pay processed $35 billion of that volume, growing 59 percent, with international Shop Pay GMV growing more than 70 percent. Shopify Capital’s gross loan receivables hit $1.6 billion at the end of 2025, up 43 percent year over year per the company’s 10-K filing.

Compare those growth rates to Subscription Solutions revenue (the SaaS plan side of the business), which grew 21 percent in Q1. The gap between 39 percent Merchant Solutions growth and 21 percent Subscription Solutions growth is the operating thesis for the entire company right now. Shopify is increasingly a financial services business that happens to ship a commerce platform, and the financial services growth is the lever that keeps overall revenue compounding at 34 percent year over year.

Here is the strategic constraint: Shopify Payments penetration is approaching a natural ceiling. Most U.S. merchants who can use Shopify Payments already do. International expansion has limits. To keep Merchant Solutions revenue growing at 39 percent or more, Shopify needs to expand the financial product surface area beyond payment processing.

Money transmitter licenses are the regulatory unlock for that expansion. They let Shopify build merchant-to-merchant payments, expanded wallet functionality, direct cross-border payouts, automated invoicing, and any number of treasury services without needing a third-party licensed party in the middle of every dollar that moves. The Q1 numbers are not a one-time outperformance. They are the demonstration that the strategy works, which is exactly why the licensing project is funded and moving fast.

Shopify obtaining money transmitter licenses does not replace Stripe; it changes which layer of the payment stack each company controls.

Today’s reality is layered. Shopify Payments is powered by Stripe’s processing infrastructure under the hood, with Stripe Payments Company acting as the licensed money transmitter and merchant funds held at Fifth Third Bank. Shopify Balance and Shopify Credit Visa cards are powered by Stripe and issued by Celtic Bank. Shopify Capital loans are originated by WebBank. Stripe’s processing rails are the operational engine; the regulated entities (Stripe Payments Company, Fifth Third, Celtic, WebBank) are the licensed parties on the regulatory side. Shopify orchestrates the merchant-facing experience.

What changes when Shopify gets its own money transmitter licenses: Shopify can step into the licensed money transmitter role itself, hold merchant funds directly, and remove a layer of partner economics from the stack on regulated money movement. The processing rails can still be Stripe (or whichever processor Shopify chooses for specific transaction types). The bank partnerships for FDIC insurance, BIN sponsorship, and regulated lending may evolve in scope but are unlikely to disappear, because the underlying banking relationships are the cheapest path to capabilities Shopify does not need to own to capture margin.

Net effect: this is Shopify moving up the regulatory stack to capture more margin on money movement, while keeping the operational partnerships that work. It is not a divorce from Stripe.

The companies also continue to partner on other fronts. Stripe co-developed the Agentic Commerce Protocol with OpenAI. Shopify and Google co-developed the Universal Commerce Protocol, which Stripe joined the tech council of in April 2026. The companies compete and cooperate at the same time, which is normal for mature ecosystem players. Treating this story as Shopify “leaving Stripe” misses the structural point: Shopify is repricing what each layer of the stack costs the merchant.

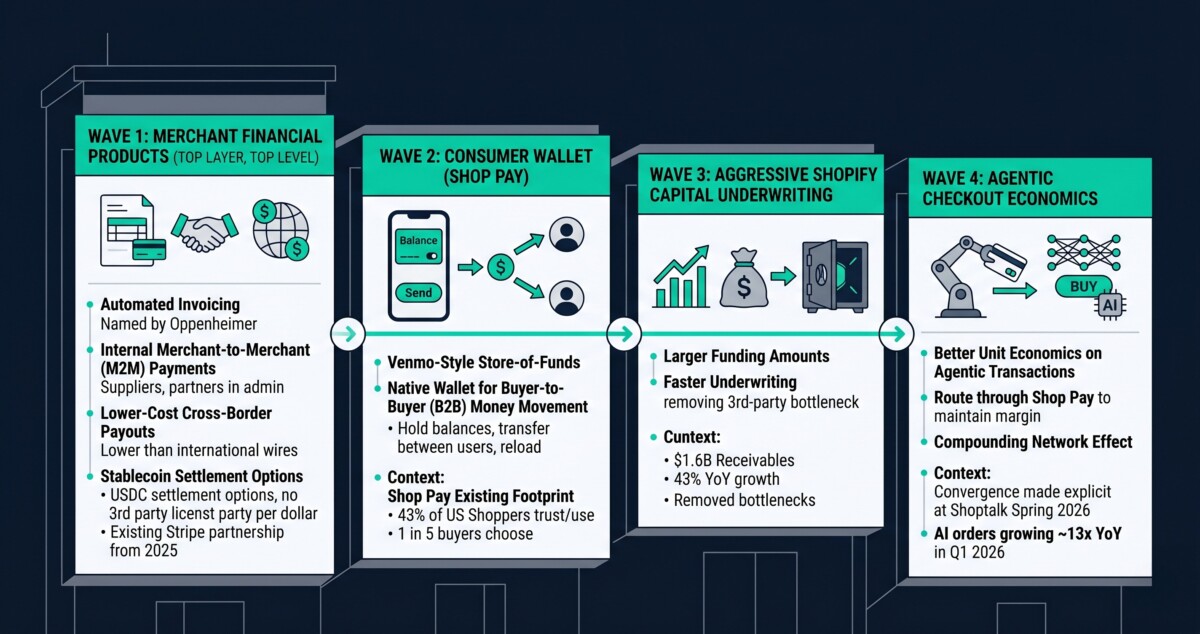

In the 12 to 18 months following full multi-state licensing, expect Shopify to roll out expanded merchant-facing financial products, more aggressive Shopify Capital underwriting, native wallet functionality competing with Venmo and Cash App for buyer-to-buyer money movement, and a tighter integration between agentic commerce checkouts and Shopify-controlled payment rails.

The first wave will be merchant products. Oppenheimer’s Ken Wong specifically named automated invoicing as a likely capability. Beyond that, expect things like merchant-to-merchant payments inside the Shopify ecosystem (paying suppliers, contractors, and partners without leaving the admin), cross-border payouts at lower cost than international wire transfers, and stablecoin settlement options that do not require a third-party licensed party for every dollar that moves. Shopify’s existing partnership with Stripe on USDC settlement (announced in 2025) gives a preview of how the company is thinking about programmable money.

The second wave will be consumer wallet functionality through Shop Pay. The “provider of prepaid access” designation explicitly enables a Venmo-style store-of-funds product where buyers can hold balances, transfer between users, and reload from external accounts. Shop Pay already has the consumer footprint, with 43 percent of U.S. shoppers trusting and using Shop Pay as a checkout method per Shopify, and 1 in 5 buyers choosing Shop Pay at checkout. The wallet layer is the natural next product.

The third wave will be more aggressive Shopify Capital underwriting. With Shopify Capital already at $1.6 billion in receivables and growing 43 percent year over year, removing the third-party regulated lender bottleneck makes faster underwriting and larger funding amounts operationally easier. Expect Shopify Capital offers to land in more merchant admins and at higher amounts.

The fourth wave will be agentic checkout economics. AI-driven orders grew nearly 13x year over year in Q1 2026, and the strategic implications for merchants are covered in the Shopify agentic commerce playbook for 2026. The long-run question for the licensing story specifically is who keeps the margin on agent-initiated transactions. Shopify-controlled payment rails plus Shopify-controlled money transmission means the platform can offer better unit economics on agentic transactions to merchants who route them through Shop Pay, which compounds Shop Pay’s network effect. The Shoptalk Spring 2026 announcements made this convergence explicit, and the money transmitter licensing is the financial layer that makes that convergence economically defensible for Shopify.

Every Shopify financial product you adopt makes leaving Shopify more expensive than the previous one, and money transmitter licensing accelerates how many financial products will be offered to you over the next two years.

Consider what changes when your payouts arrive in Shopify Balance instead of an external business bank account. Switching costs include moving direct deposits, vendor ACH connections, the cashback you have earned on the Shopify Credit Visa, the APY rewards accumulating on your balance, and the bookkeeping integrations pointed at the Shopify Balance feed. None of these are large individually. They compound.

Consider what changes when you take a Shopify Capital loan. Per Shopify’s published terms, you cannot deactivate Shopify Payments until the loan is fully repaid. That is not hypothetical lock-in; it is contractual. You are operationally bound to Shopify Payments until the balance is zero, which can be 18 months or more.

Consider what changes when Shop Pay becomes the primary post-purchase experience for your buyers. Order tracking happens in the Shop app, and repurchase rates run 9 percent higher for Shop app users per Shopify’s own data, which is real value. But the customer relationship shifts toward the Shop app and away from your owned channels. The relationship is increasingly intermediated by Shopify infrastructure.

Consider what changes when agentic checkouts route through Shopify-controlled rails. Your conversion data, attribution, and customer data all flow through Shopify infrastructure first.

The merchants who scaled cleanly through the $500K to $2M stage made financial product decisions deliberately, asking each time whether the choice made their business more or less portable in three years.

This is not anti-Shopify. Shopify Payments is genuinely the right choice for almost every merchant under $5M. Shopify Capital can be the right choice when capital costs less than the opportunity it funds. Shop Pay drives real conversion lift competitors cannot match. The point is not to refuse these products. The point is to know what you are trading for them.

The pattern across hundreds of merchant conversations is consistent. The operators who run into trouble at the $500K to $2M stage are usually the ones who accepted every product reactively. The operators who scaled cleanly were deliberate, knowing which products they insourced to Shopify and which they intentionally kept portable.

At your stage, the right move differs: for $0 to $500K stores it is awareness, for $500K to $2M stores it is documenting what is portable, for $2M to $10M stores it is a quarterly platform-dependence review, and for $10M+ operators it is a financial products audit before the back half of 2026.

For Starting stores ($0 to $500K), use Shopify Payments, use Shopify Balance if the cashback fits your spending, and skip Shopify Capital unless you have genuinely modeled the cost against alternatives. Premature complexity at this stage is the most reliable way to slow yourself down. Shopify is the right platform to grow on. Just keep your customer email list, your business banking, and your vendor relationships in places that are not Shopify infrastructure.

For Scaling stores ($500K to $2M), document what is currently portable. Specifically: your customer email list lives in your ESP and your own CRM (not just the Shop app); your vendor payment information lives in your accounting system independent of Shopify Bill Pay; your business banking lives at a real bank with FDIC insurance independent of Shopify Balance. When you receive a Shopify Capital offer, compare it against revenue-based financing alternatives before accepting. The dependence implications are always meaningful even when the cost difference is small.

For Scaling stores ($2M to $10M), run a quarterly platform-dependence review with your finance lead. Ask one question: what would it cost us to move off Shopify in 12 months if we had to? Track that number. Make sure you are not accepting financial products faster than you are reducing operational dependence elsewhere. The point is balance, not refusal. A merchant who insources Shop Pay rails for 60 percent of orders should be deliberately maintaining alternative checkout options for the other 40 percent.

For Mid-market and above ($10M+), audit your full financial product stack before Q4 2026. Map every Shopify product you use, every vendor relationship that runs through Shopify rails, every contract that assumes Shopify infrastructure. Build the spreadsheet. Update it quarterly. The decisions you make in late 2026 about which products to insource and which to keep external will compound for years. Pair this audit with a Shopify Commerce Readiness Tool scan so the diagnostic covers both the merchant-facing layer and the strategic dependence layer.

For most Shopify merchants, the immediate impact in 2026 is minimal: your payments will still process, your payouts will still arrive, and your existing Shopify Capital balance will continue to work the same way. The strategic impact rolls out over the next 18 to 24 months as Shopify completes state-by-state licensing and uses its new regulatory standing to launch direct merchant financial products. Expect new offerings in your admin, including expanded Shop Pay capabilities, more aggressive Shopify Capital underwriting, potential merchant-to-merchant payment options, and possibly a wallet-style consumer product comparable to Venmo or Cash App. The right move now is to be aware and make intentional decisions about which products to adopt.

Shopify Payments processing fees are unlikely to drop in 2026, but the licensing changes give Shopify the regulatory standing to offer differentiated pricing on specific transaction types over time. The current processing rate is set by competitive dynamics with Stripe-powered alternatives and PayPal, not by who holds the underlying money transmitter license. What is more likely to change is the economics of newer transaction types like agentic commerce checkouts, cross-border payouts, merchant-to-merchant transfers, and stablecoin settlement, where Shopify can offer better pricing because it no longer needs to share margin with a third-party licensed money transmitter. Watch for new transaction types with attractive pricing first, not changes to your standard credit card processing rate.

No, Shopify becoming its own money transmitter is not a reason to stop using Shopify Capital, but it is a good moment to reconsider how you evaluate Shopify Capital offers against alternatives. Shopify Capital terms are typically competitive for merchants who need fast funding without traditional credit checks, and the underlying lender (currently WebBank) is unlikely to change in the near term. The strategic consideration is unchanged from before the licensing news: every active Shopify Capital balance locks you to Shopify Payments until the loan is fully repaid, which has dependence implications regardless of who holds the money transmitter license. Compare Shopify Capital against revenue-based financing, traditional lines of credit, and supplier credit before accepting any offer.

Shopify obtaining money transmitter licenses is not Shopify replacing Stripe; it is Shopify changing which layer of the payment stack it controls directly. Shopify Payments is currently powered by Stripe’s processing infrastructure, with Stripe Payments Company acting as the licensed money transmitter and funds held at Fifth Third Bank. Money transmitter licenses allow Shopify to step into the licensed-entity role itself and hold funds directly, while the processing rails can still be Stripe (or whichever processor Shopify chooses for specific transaction types). Stripe and Shopify continue to partner on agentic commerce protocols, B2B payment infrastructure, and other initiatives. The two companies compete and cooperate simultaneously, similar to other long-term technology partnerships in the ecommerce stack.

Shopify currently holds money transmitter licenses in 18 states plus Puerto Rico, with applications under review in the remaining jurisdictions, including California and New York. Full nationwide coverage is most likely to be complete by mid-2027 to early 2028. Money transmitter licensing in the United States is regulated state-by-state, with each application typically taking 6 to 18 months, depending on the state’s net worth requirements, surety bond requirements, background check timelines, and review backlogs. Larger states with stricter regulations, like New York (which has its own BitLicense framework for digital asset activity) and California, typically take longer than smaller states. No public timeline has been provided by Shopify, but the operational hiring patterns suggest the company is resourcing for a multi-year completion.