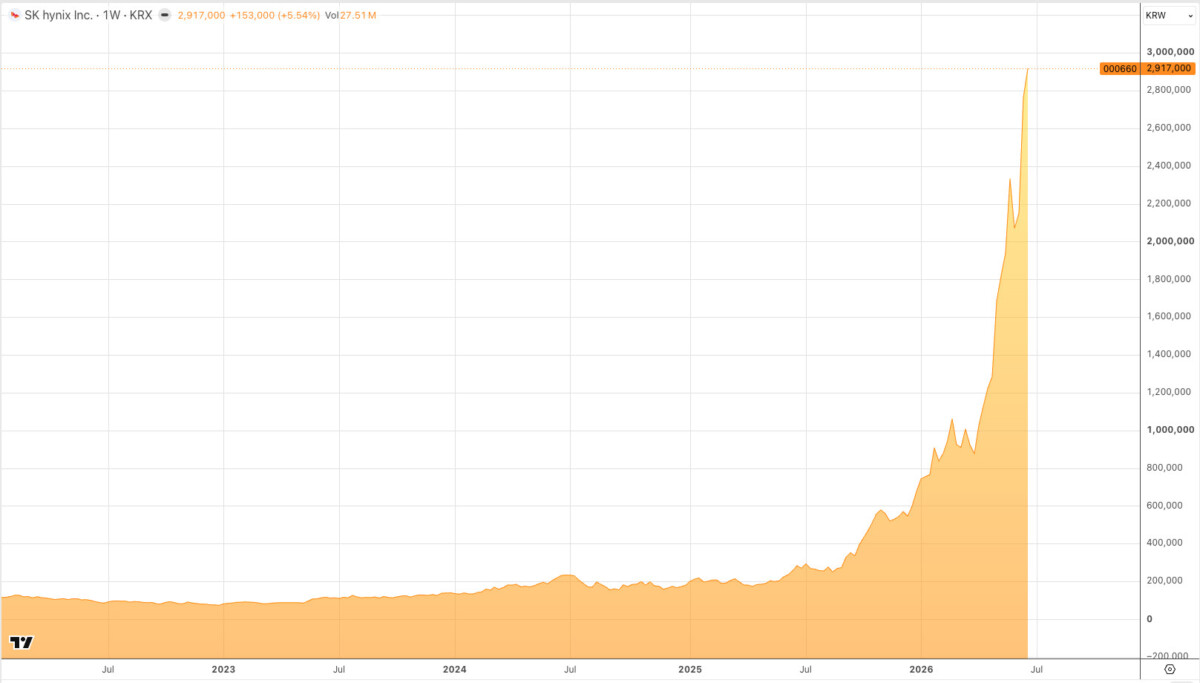

SK hynix overtook Samsung Electronics as South Korea’s most valuable public company in 2025-2026 by dominating the high-bandwidth memory market that powers Nvidia’s AI accelerators. With 61% global HBM market share, a planned $29.6 billion NASDAQ listing, and shares up over 300% since the start of the year, the company has become the semiconductor industry’s defining winner of the AI infrastructure boom.

Samsung spent two decades as South Korea’s most valuable company. It took SK hynix less than two years of AI-driven HBM demand to end that run — and the gap is still widening.

Just a few years ago, Samsung Electronics’s dominance of the South Korean stock market seemed unassailable. For two decades, the company held the title of the country’s most valuable publicly traded corporation, serving as a symbol of South Korea’s technological leadership. However, the AI boom is rapidly reshaping the competitive landscape, even among the industry’s largest players.

SK hynix, long overshadowed by its larger rival, has emerged as the market’s new favorite. The company has now surpassed Samsung in market capitalization and is preparing to reinforce that momentum with a major listing on the U.S. capital markets.

According to the filing, SK hynix plans to issue nearly 17.8 million new shares on NASDAQ in the form of American depositary receipts (ADRs). The offering could raise approximately $29.6 billion and is expected to influence NASDAQ index futures. The announcement immediately boosted investor sentiment, sending SK hynix shares up another 11% in South Korea.

This move is about far more than raising capital. American listing is strategically important because the country’s largest technology companies, including Microsoft (NASDAQ:MSFT), Nvidia (NASDAQ:NVDA), Amazon (NASDAQ:AMZN), Google (NASDAQ:GOOG) are among the world’s biggest buyers of AI memory and advanced semiconductor solutions.

The funds raised help finance several major projects. SK hynix is already building a $4 billion advanced memory testing and packaging facility in Indiana, while simultaneously expanding manufacturing capacity in South Korea. As AI-driven demand continues to outpace supply, semiconductor companies are racing to invest in new production infrastructure.

Investors appear eager to fund these ambitions. Since the beginning of the year, SK hynix shares have grown by more than 300%, lifting the company’s capitalization to roughly $1.35 trillion. That surge allowed the memory maker to overtake Samsung Electronics for the first time and became South Korea’s most valuable public company.

The turnaround is particularly remarkable given the company’s history. In the early 2000s, SK hynix faced a severe financial crisis, narrowly avoided being acquired by Micron Technology, and watched its share price collapse to historic lows. Today, it ranks among the world’s most expensive technology companies, placing 13th globally by market capitalization.

The main driver of this extraordinary growth has been high-bandwidth memory (HBM), which has become one of the critical resources of the AI era. HBM chips power Nvidia’s AI accelerators and other advanced computing systems used to train and run modern AI models.

By the end of last year, SK hynix controlled about 61% of the global HBM market, compared with 17% for Samsung and 21% for Micron. Its early commitment to the technology positioned the company at the center of the semiconductor industry’s largest investment cycle.

HBM already accounts for about 40% of SK hynix’s revenue. However, management also sees strong opportunities in expanding production of DDR5 and LPDDR5 memory. The rationale is straightforward: in operating margins for conventional server memory could approach 90% over the coming year. In addition, long-term DRAM supply agreements with major customers, including Microsoft, provide stable cash flows and reduce the need to shift all production capacity toward HBM4.

That strategy stands in sharp contrast to Samsung’s approach. Viewing its weaker position in HBM as a strategic vulnerability, Samsung is accelerating the irollout of next-generation memory products while rapidly expanding production capacity in an effort to close the gap.

For now, however, SK hynix appears to be the AI boom’s biggest financial winner. The company not only dominates the industry’s most supply-constrained memory segment but is also poised to raise tens of billions of dollars in the world’s largest capital market. At the same time, management has demonstrated a willingness to prioritize profitability over maximizing market share.

That is why SK hynix’s planned Nasdaq listing represents far more than another equity offering. It underscores a broader shift in the semiconductor industry: memory has become one of the digital economy’s most strategic assets, and memory manufacturers are increasingly commanding the attention of global investors alongside the world’s leading AI developers.

SK hynix overtook Samsung primarily because of its dominant position in high-bandwidth memory, the specialized semiconductor that powers Nvidia’s AI accelerators and other advanced AI computing systems. By the end of 2025, SK hynix controlled approximately 61% of the global HBM market compared to Samsung’s 17%. As AI infrastructure investment accelerated, demand for HBM outpaced supply, and SK hynix’s early commitment to the technology translated directly into revenue growth, margin expansion, and a share price increase of more than 300% since the start of 2026. Samsung, despite its broader semiconductor capabilities, was slower to build HBM manufacturing capacity and has been working to close that gap.

High-bandwidth memory is a type of semiconductor that stacks memory chips vertically to deliver significantly higher data transfer speeds than conventional DRAM, which is critical for AI workloads that require moving large amounts of data rapidly between memory and processing units. Nvidia’s most advanced AI accelerators, including the H100 and its successors, use HBM to achieve the performance required for training and running large AI models. Without sufficient HBM supply, the AI infrastructure buildout slows. That dependency is why HBM has become the semiconductor industry’s most supply-constrained resource and why SK hynix’s 61% market share in this segment translates directly into pricing power and investor attention.

SK hynix plans to issue approximately 17.8 million new shares on NASDAQ in the form of American depositary receipts (ADRs). The offering could raise approximately $29.6 billion, which would make it one of the largest technology listings in recent memory. The capital is earmarked for major infrastructure projects, including a $4 billion advanced memory testing and packaging facility in Indiana and expanded manufacturing capacity in South Korea. The listing also gives SK hynix direct access to U.S. institutional investors and greater visibility with the American technology companies that are its largest customers.

SK hynix is running a dual-track strategy that balances HBM leadership with high-margin conventional memory products including DDR5 and LPDDR5, supported by long-term supply agreements with customers like Microsoft. Samsung, by contrast, is accelerating production across next-generation memory categories in an effort to close its HBM gap. The core difference is that SK hynix has prioritized margin quality alongside volume, while Samsung is emphasizing production scale and speed to market. Operating margins for conventional server memory could approach 90% over the coming year, which means SK hynix’s broader portfolio strategy is designed to generate strong returns even as HBM demand fluctuates.

SK hynix’s rise signals that the AI supply chain has real constraints at the memory layer, not just the chip design layer, and those constraints influence the cost, availability, and development pace of the AI infrastructure that powers the tools businesses use. When HBM supply is tight, AI accelerator production slows, which affects how quickly cloud providers can expand AI capacity and, downstream, what AI-powered services cost to run. For founders and operators evaluating AI tool roadmaps or infrastructure costs, understanding where the supply bottlenecks sit in the AI stack — and which companies control them — provides useful context for planning over a 12-24 month horizon.