Fashion is constantly evolving.

Seasons change. Tastes transform. Fads come and go.

Ruled by subjectivity, risk weaves itself into the fashion industry … blessing one moment. Cursing the next.

And it’s not just a matter of style.

How fashion ecommerce brands operate is constantly evolving too. New technologies, shifting markets (at both geographic and economic levels), plus the shadow of profitability.

For ecommerce, COVID-19 thrust a decade of growth into a single year. It’s also overturned traditional loyalties and given birth to a new wave of direct-to-consumer winners.

Threading the needle calls for a clear understanding of the 10 trends shaping ecommerce fashion.

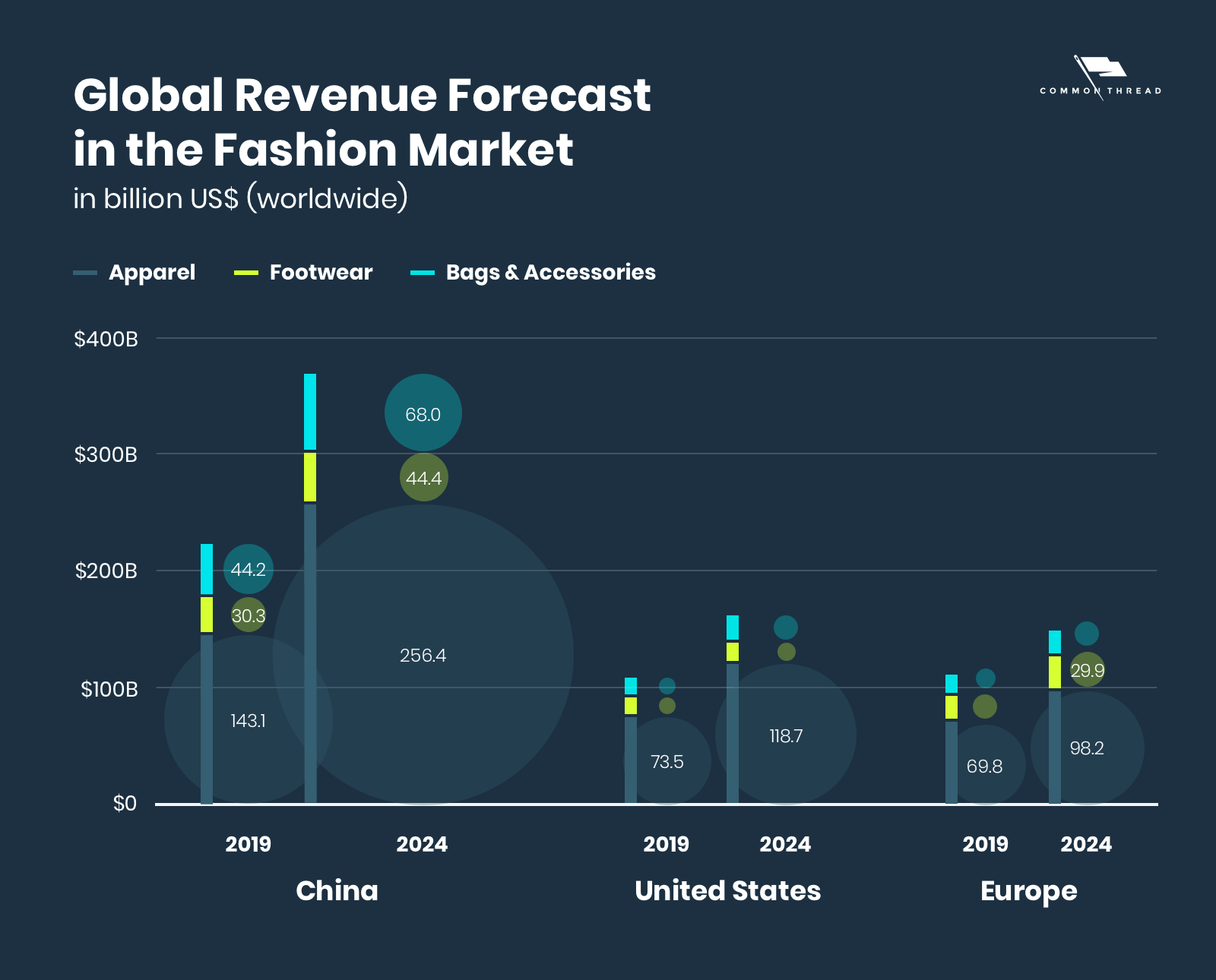

The business of fashion is more than big; it’s the biggest of the big.

With a global market value of $759.5 billion in 2021, apparel, accessories, and footwear are the number one ecommerce sector in the world.

Over the next five years, online fashion’s 7.18% compounded annual growth rate will put the industry at +$1.0 trillion.

Fueling this growth are two factors: penetration rates — as defined by “the share of active paying customers” — and ecommerce’s share of retail fashion.

Estimates project an overall increase in ecommerce penetration from 46.6% this year to 60.32% by 2024. Applied to the three major fashion segments:

Though more modest, that represents a total market share lift from 21.03% in 2020 to 23.66% in 2023.

Geographically, consumption tilts heavily toward China; its $284.3B in 2020 sales outpacing the next four countries combined:

Moving forward, China’s dominance will only intensify …

International data should not be used to downplay North America and Europe’s role in shaping worldwide preferences. Nor the opportunities still emerging domestically.

Globally, coronavirus hit online apparel and accessories hard. Conversely, eMarketer reports 9% YoY growth in the US and a step-change in its percentage of total retail sales from 26% to 37%.

In addition, individual US consumers already out spend their Chinese and European counterparts as evidenced by average revenue per user (ARPU).

That gap is expected to widen substantially:

Of course, aggregate data can be a tricky thing. Especially during a global pandemic.

Against eMarketer’s +9% YoY change, Statista shows slight declines in 2020 versus 2019. Vertical-by-vertical examinations in the US reveal marked disparities, with luxury products and accessories (i.e., watches, jewelry, luggage, and bags) bearing the brunt of losses …

The good news is that compounded annual growth rates over the next five years are up and to the right for fashion at large as well as every subcategory.

In other words, no matter what source you turn to the prognosis is the same: either 2020 will end with online fashion in the black or its losses will rebound in 2021.

With projections to benchmark your own growth, one final piece of foundational data must be attended to before looking at examples of these ecommerce trends in action.

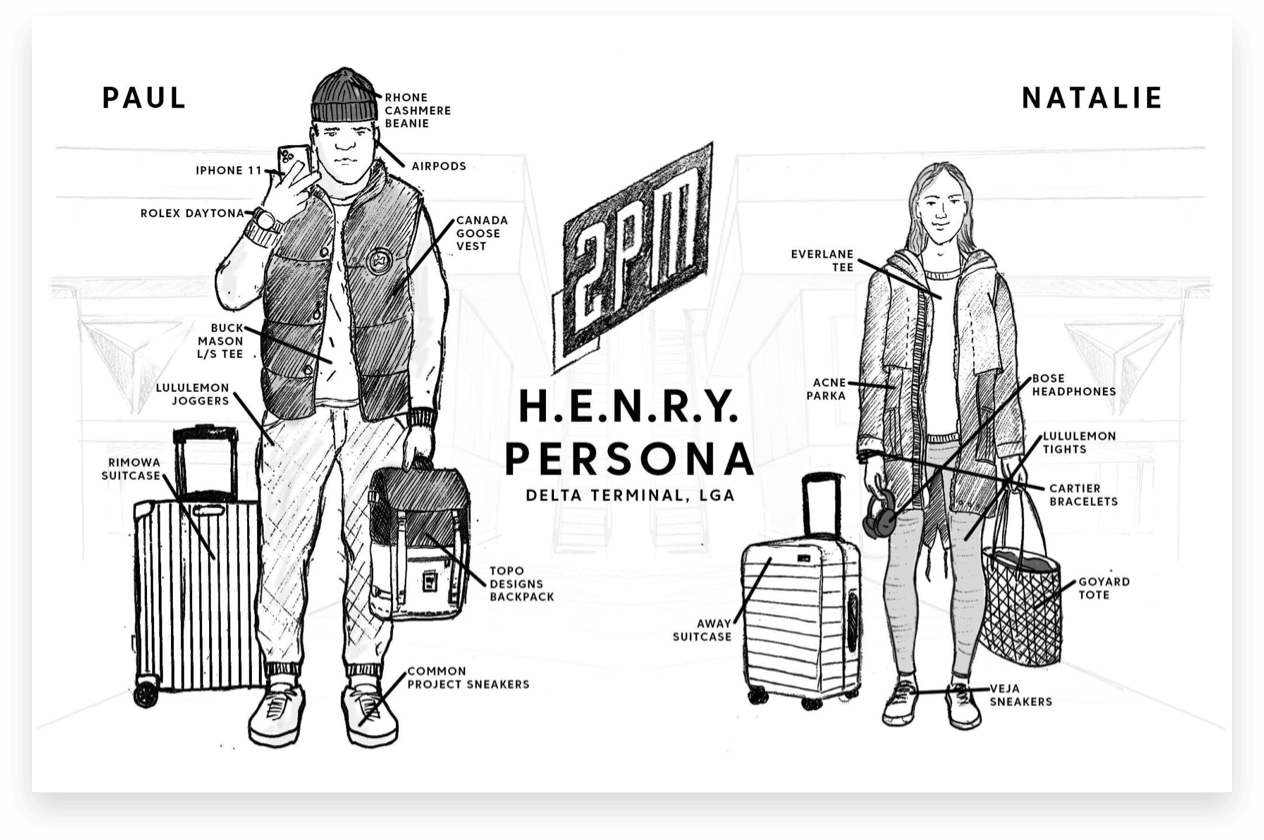

Call it H.E.N.R.Y. (high earners not rich yet) versus C.A.R.L.Y. (can’t afford real life yet), “Generation C” versus “Generation N,” new-luxury versus dollar-shoppers … or simply brands versus commodities.

Regardless of the name, the divide between haves and have nots has never been more stark. Or, rather, between those willing to pay for appearances (H.E.N.R.Y.) and those who don’t have the luxury (C.A.R.L.Y.).

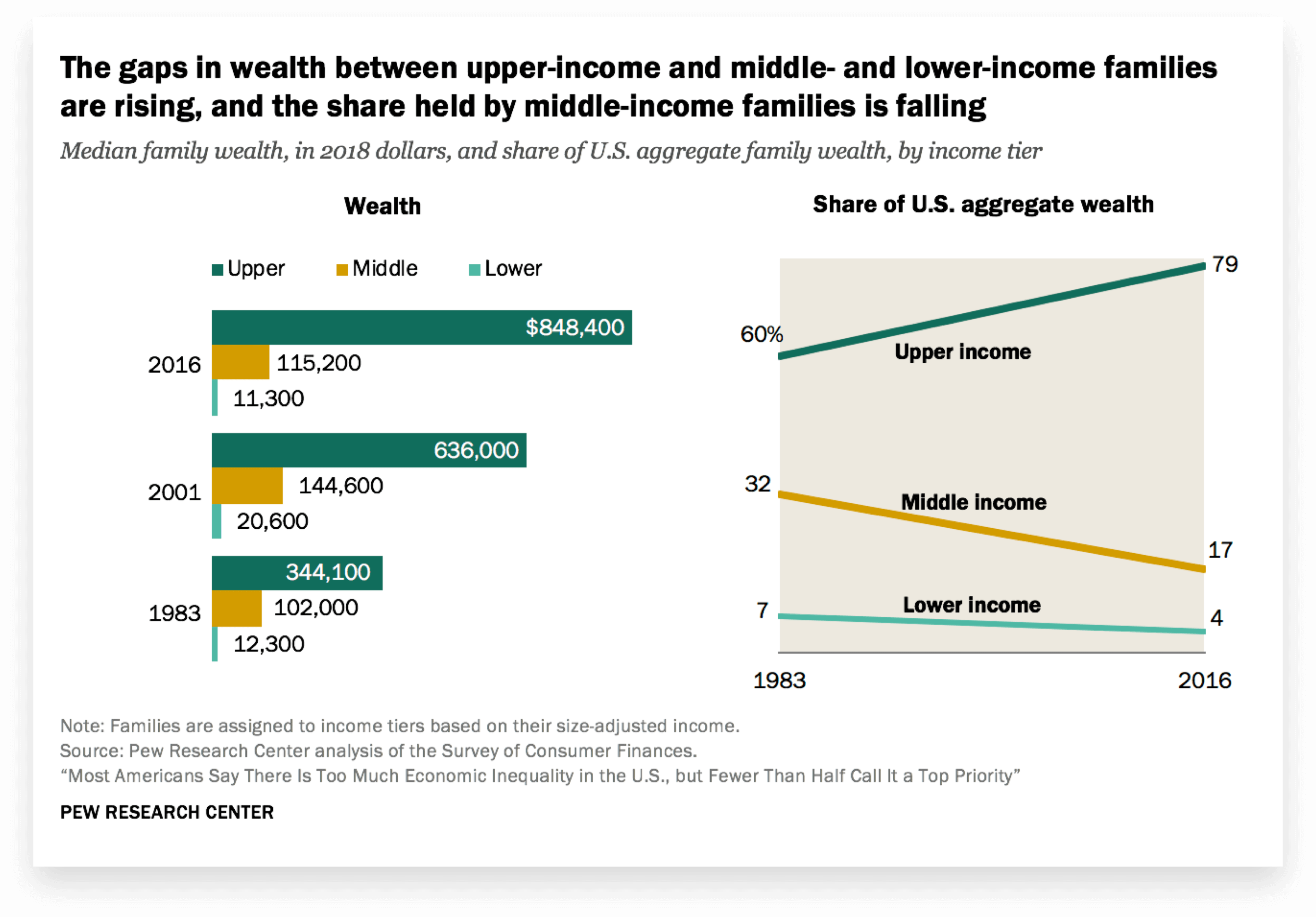

Economic gaps are likewise bifurcating commerce. Recent history is littered with mid-market mishaps — both online and off. In the US, income and wealth gaps have both deepened over the last decades:

Shopping habits reflect these divides; particularly retail behemoths aimed at cost-conscious consumers as well as their fast-fashion equivalents.

Regardless of the generation, superstores, discount stores, and warehouse clubs have become de facto choices. Department stores and local boutiques, in last place.

The same is true online; most notably, Amazon and enterprise online business’ lion share of the market.

No industry bears this mark more clearly than fashion.

And no sub-category should be more alert to its effects than DTC.

As middle-class consumers either disappear, seek experiences (over things), or reach upward beyond their means … brands must likewise make a choice.

Up-market. Down-market. Or languish in-between.

From brand to merchandising, advertising to advocacy, even pricing to loyalty, the implications of this choice affect every other trend.

Perhaps nowhere is it more relevant than the next.

The struggle of profitability isn’t new. Even before coronavirus, its casualties were mounting.

DTC darlings like Outdoor Voices, Everlane, AWAY, and Bonobos have all found themselves beneath headlines with one theme: at scale, the economics of ecommerce don’t work.

At the same time, outliers have emerged.

Among the 435 companies listed in 2PM, Inc.’s DNVB Power List, 170 belong to the apparel or accessories category. The next largest: health and wellness with 94.

The Top 20 Apparel or Accessories Digitally Native Vertical Brands

Though not ranked in the top 20, Gymshark is perhaps the most instructive. After selling 21% to General Atlantic in Aug at a +£1 billion valuation, recent news majored on its unicorn status.

Typically cited strengths include a healthy mix of paid and organic social media, influencer marketing, and IRL events … all anchored in unifying its community.

Less lauded in the mainstream was the brand’s negative cash conversion cycle. Gymshark’s financial filings revealed not only operating profits at +£18 million and cash reserves of +£30 million but also shrewd payment terms with suppliers.

Cash conversion cycle (CCC) is a measure of how many days it takes for a biz to turn invested cash (usually purchased inventory) back into cash in its bank account.

The formula is: Days Inventory + Days AR – Days AP

— Jay Vasantharajah (@jayvasdigital) July 16, 2020

“A negative cash conversion cycle means that their vendors are financing their operations. As their sales grow, their cash balance magically increases instantly.”

Gymshark’s surface-level tactics certainly played a major role. And yes, we’ll examine a number of those trends as manifested in other fashion brands below.

Still, the company’s financial savvy fueled rapid growth without demanding the rock-and-hard-place choice many cash-strapped DTC brands face: long-term debt or pre-mature VC investment.

Vasantharajah’s article (linked above) provides a handful of steps to negotiate terms. The point, however, isn’t necessarily to go forth and replicate.

Instead, it’s a call to reorient fashion from frontend flare to backend books.

An interlude on profitable growth …

Despite complexity, profitable growth comes down to four metrics: visitors, conversion rate, LTV (your cash multiplier), and variable costs.

Without hyperbole, that single equation is the future of ecommerce; fashion or otherwise.

As an agency, it’s fundamentally shifted how we structure client relationships. It’s also come to life in two resources. One, a guide on the ecommerce business strategies derived from the equation.

And two, this tutorial detailing its development and implementation:

Given fashion’s focus on self-expression, it makes sense that modern fashion consumers actively seek personalized experiences.

This goes well beyond the typical personalization techniques that have become status quo by today’s standards. Things like including the customer’s name in your emails or delivering product recommendations based on their purchase history are table stakes.

Hyper-personalization digs into the customer’s behaviors, preferences, and purchase history to determine how best to deliver value to them moving forward.

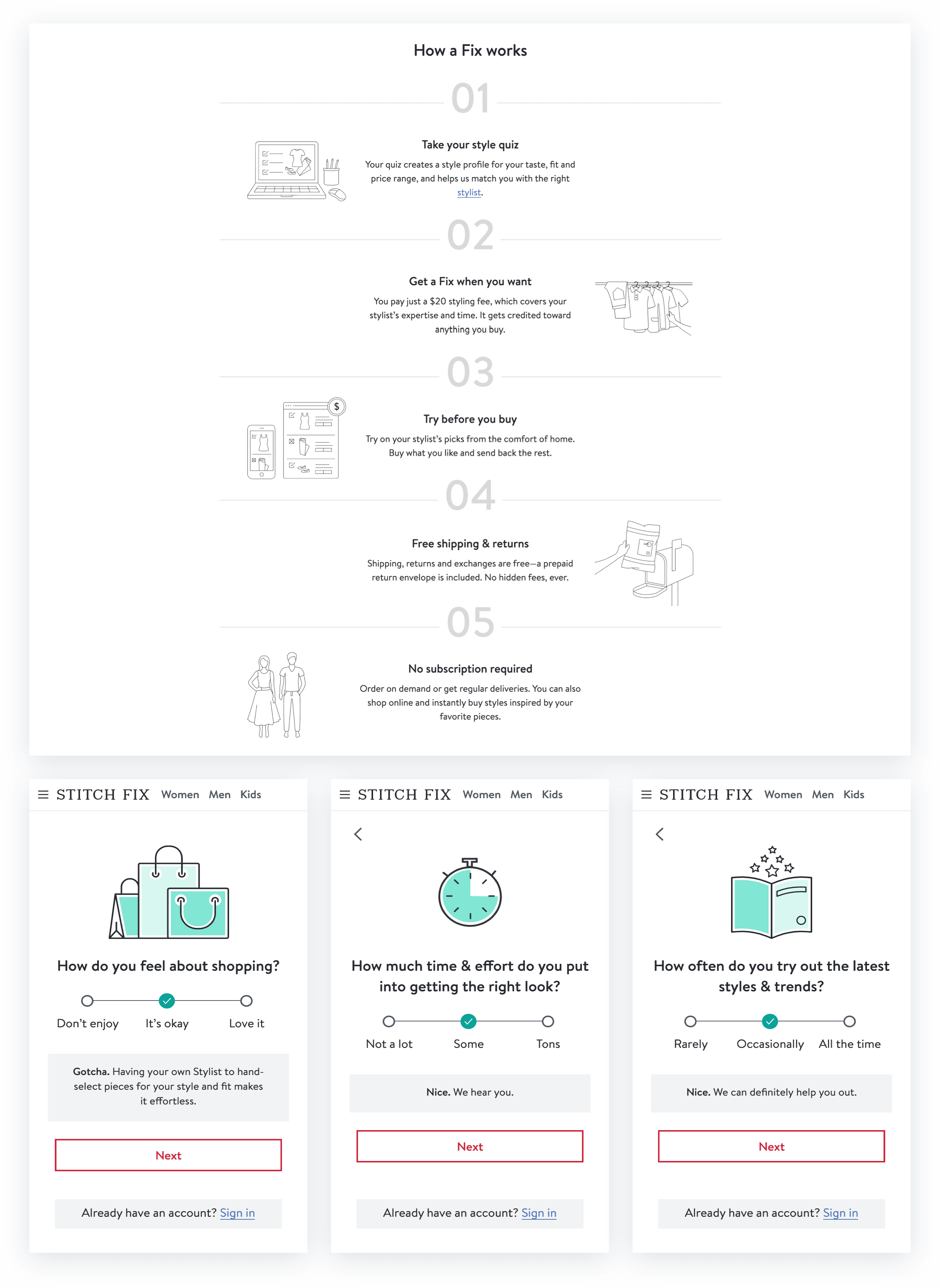

The exemplar of this trend is Stitch Fix. Since its inception in 2016, the DTC startup has grown in value to roughly $2.9 billion as of June 2020.

Through the use of artificial intelligence and machine learning, Stitch Fix determines the exact products to deliver to its individual customers on a subscription basis.

That level of personalization may feel out of reach. Thankfully, the principles behind it are anything but.

For starters, quiz funnels have become a staple of new customer acquisition for Common Thread Collective’s fashion clients as well as our in-house brands.

Tools like Octane AI or Typeform (if you really need to be scrappy) make frontend creation easy. They also make backend integration smooth with email marketing platforms like Klaviyo. With each, direct access to your product catalogue and customer information (e.g., Shopify, Magento, or WooCommerce) must be accessible.

Onsite tools such as Nosto take hyper-personalization a step further, delivering dynamic onsite content to users based on their engagement history. This goes for product recommendations, page copy, and more.

With the above in mind, it should be no surprise that multi-channel marketing has become a necessity. Terms like multi-channel and omni-channel often feel cloaked in complexity. Especially for growing retailers.

Put simply, multi-channel ecommerce means establishing a consistent and purchase-centered experience on the digital spaces consumers inhabit. It need not span the internet.

Nor does it demand being everywhere for everyone.

Instead, savvy brands expand one channel at a time: mastering and prioritizing their presence along four frontiers …

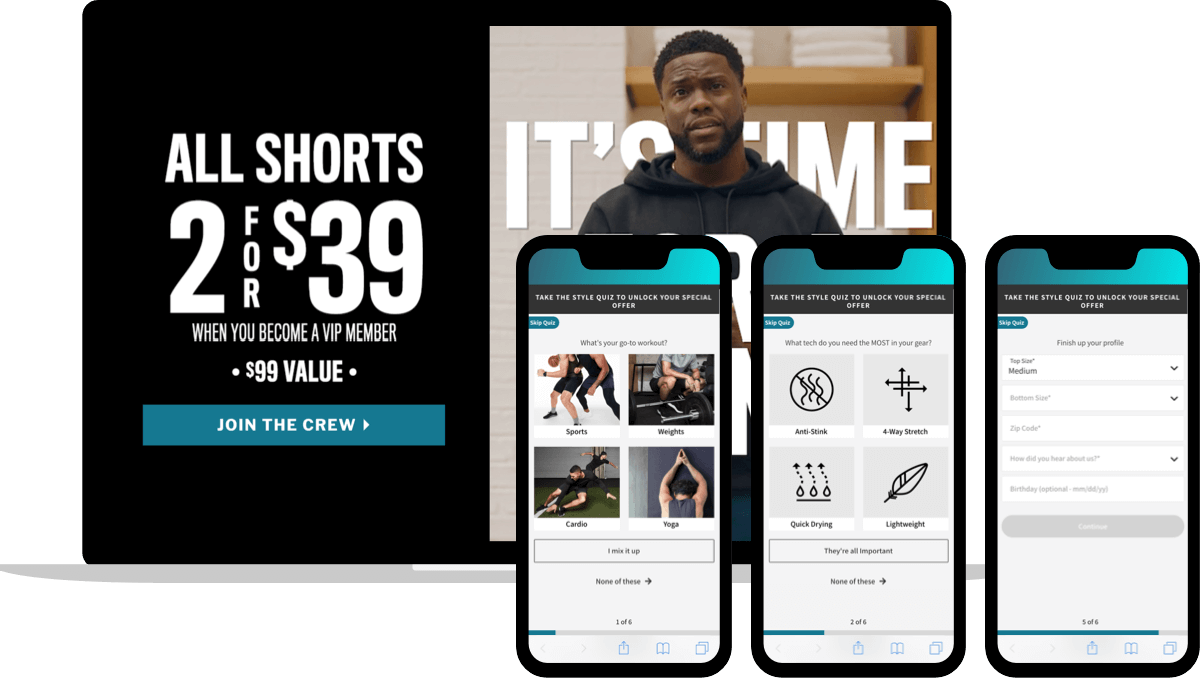

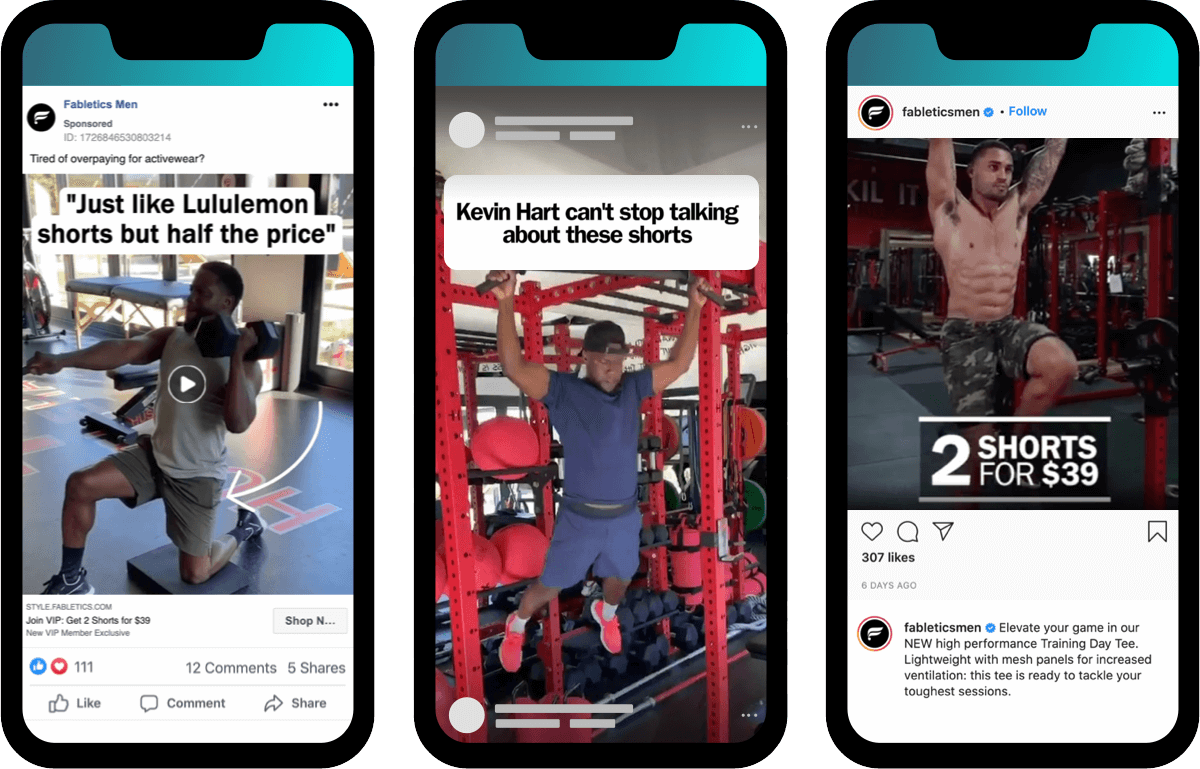

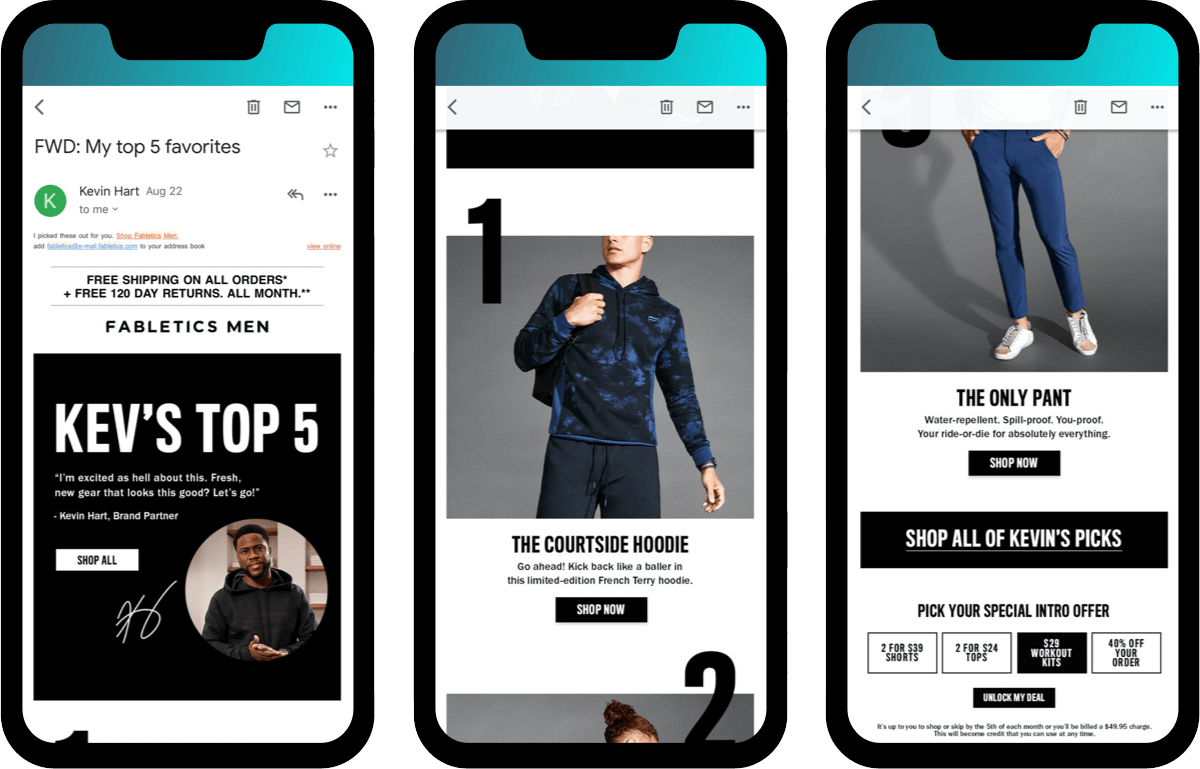

As a guide, consider Fabletics.

Recently, the brand launched a straightforward sales campaign with Kevin Hart. It began with a series of ads run natively through Kevin’s Instagram, led to a custom landing page (rather than the homepage, product page, or collection page), and culminated in a six-part quiz:

Simultaneously, Fabletics released paid and organic content through its own social-media accounts, also featuring Kevin as well as competitive messaging:

The campaign’s crowning glory appeared on what is often considered the least “cutting-edge” channel: an email from Fabletics sent through Kevin Hart’s name:

For all its seeming complexity, the approach essentially runs on three channels: Facebook, onsite (through a custom landing page and quiz), and email.

But because they interlock with a consistent message, those channels immerse their audience.

Lifestyle accessory brand, Dorsal, does something similar: anchoring its spend on Facebook and Snapchat, then extending into halo efforts on …

In addition to enhancing the customer experience for their current audience, this allows fashion businesses to expand intentionally.

Whether targeting new audiences, experimenting with new social-media platforms, or testing new creatives – multi-channel marketing is a key to growth in the fashion industry.

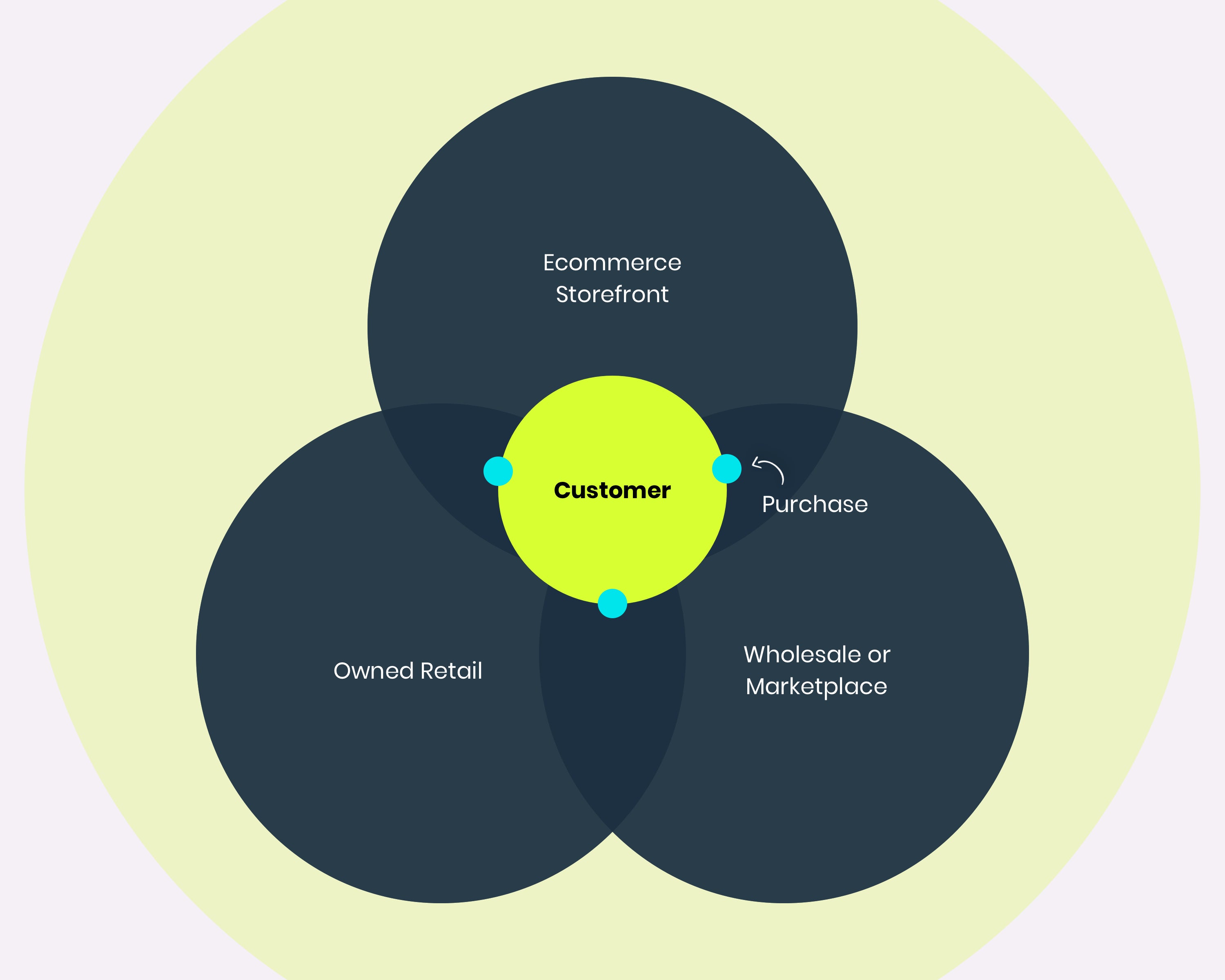

Where multi-channel connects digital experiences, omni-channel bridges the online-to-offline divide through a “single view” of customers (i.e., data) with three points-of-purchase:

Numerous born-online fashion labels have already proven the value of maturing into owned retail. Chief among them, names like Lululemon, Happy Socks, UNtuckit, and Rhone.

Shoe brand APL (Athletic Propulsion Labs) inverted that traditional path by starting its journey in luxury retailers, expanding into online DTC three years ago, and then establishing its flagship store in late 2019.

Even amidst COVID-19, DNVB juggernaut Pura Vida Bracelets made its groundbreaking announcement.

Why? Because in addition to creating a cohesive customer journey, omni-channel operations allow fashion brands to create tactile customer experience.

As Nate Checketts, Rhone’s co-founder and CEO, explains: “While transactions continue to scale and tilt towards seamless digital environments, the impetus for transactions are influenced by IRL offline.”

For Rhone, as with most apparel, that “impetus” includes (1) what customers currently own and love, (2) what friends or family own and talk about, and (3) in-person, in-store interactions.

What report on ecommerce fashion trends would be complete without predictions?

Rather than peer into the future through hazy buzzwords, instead let’s hone in on three problems and three predictions … from three leaders at the forefront.

Despite feature releases, PR, and new integrations, native commerce — i.e., buying inside social-media platforms like Facebook and Instagram — has had a tough go of it.

At best, consumers are still getting used to the idea of making purchases directly through social media. At worst, it’s a losing battle that won’t be won for at least another generation.

Marco Marandiz, Ecommerce DTC Strategist

“I see a big transition from the website being the primary channel for how you generate transactions. Moving forward, we’ll see a lot more drops as a business model, a bigger part of the revenue mix for direct-to-consumer businesses.

“Websites will become less relevant and social media channels — TikTok, Instagram, Twitter, YouTube — those are going to be far more powerful for driving sales directly to a specifically built site to make a sale. There won’t be the whole lifestyle photography and product descriptions and all of that stuff.

“There’ll be a shift towards using social media channels as your landing page and very simple transactional experiences for commerce. Maybe that’s not ‘DTC 3.0,’ but it’s the next iteration because most people are deciding to buy things when they see the ad, when they see the influencer, when they see the content, that’s when they make the decision to purchase.

“If someone’s already bought-in on an influencer, already bought in that this celebrity is going to sell me this hoodie, then just let me buy it.”

According to a July 2020 survey from Qubit, 37% of consumers shop with more brands than they did a year ago — and 46% are less loyal to brands than they used to be. What’s more, fully 75% of Americans have changed brands during the pandemic.

At the same time, 70.6% of fashion consumers say they make purchases on company websites instead of third-party sellers.

Consumers don’t mind being loyal — they just need to have good reasons.

Jeremy Cai, CEO & Founder of Italic

“Primarily relevant for brands looking to scale: you need to be realistic in looking at your business from an objective and quantitative lens.

“Invest in reporting early on and develop competency around understanding and dialing in the metrics that matter for your business on a cohort basis. The sooner you do this, the better equipped you’ll be to answer how to grow your business. Don’t put this off.

“Let’s say you sell your hero product for $100 and your contribution margin is $50, and let’s say you were acquiring early customers at $30 on Facebook, that’s great, double down. But once your CAC has grown to $60, it’ll be too late to course-correct.

“What you have to know is how much those customers who bought your hero product — and any other leading products — are worth to you month after month. Not over a lifetime, but inside timetables that feed your cash flow.

“Economies of scale are purely theoretical in DTC and you need to invest in becoming a data-driven organization early on. The radical part of Italic’s model is that we get to prioritize our members’ happiness by making retention our driving metric.”

As ecommerce adoption escalates and first-time shoppers turn online, a chief danger is losing intimacy. Retail can forge relational experiences, but customer support is often the only option for online brands. Particularly, immediate support — before, during, and after a purchase.

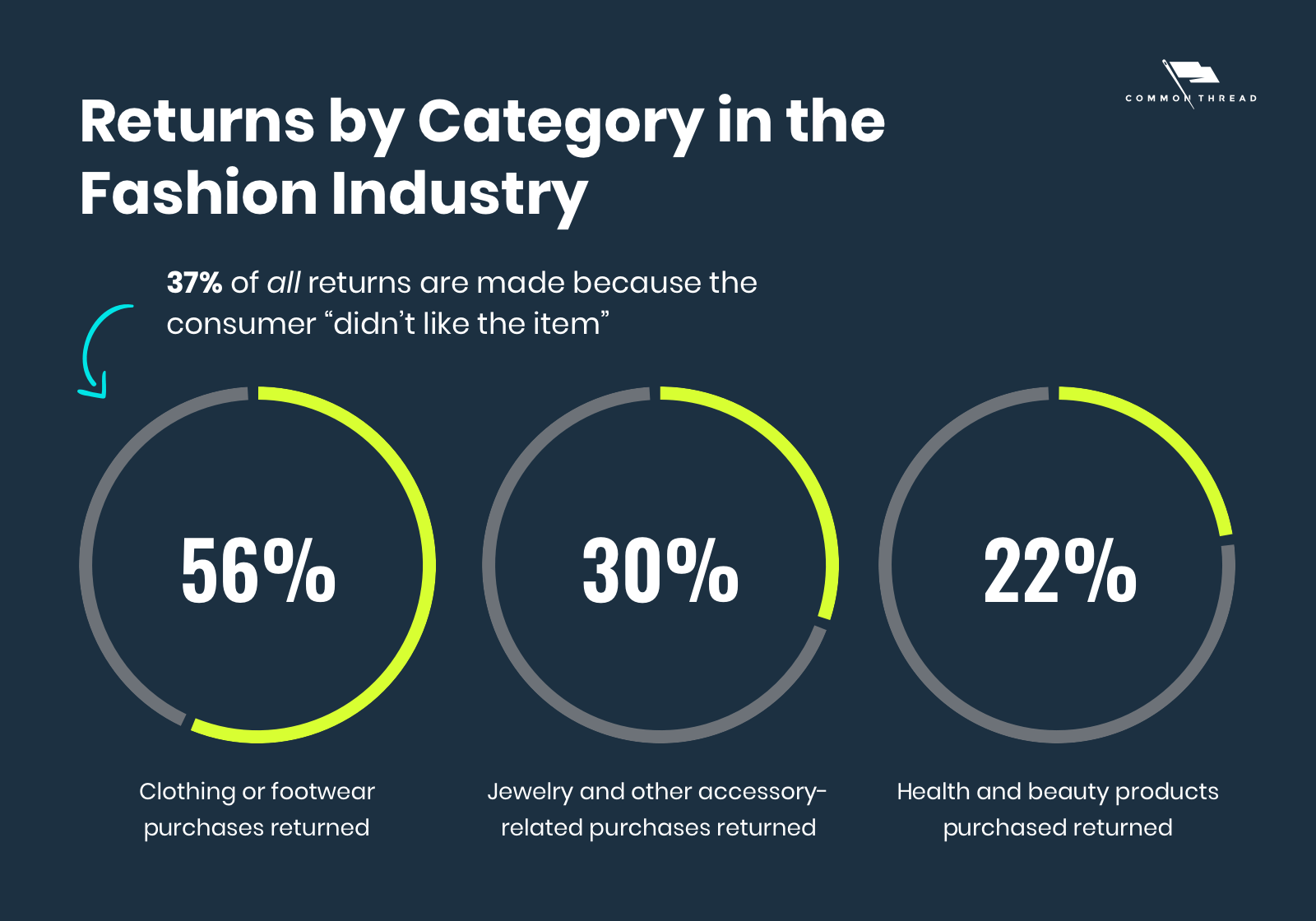

Rising return rates are another danger that loom large over online fashion:

Vanessa Skaggs, Marketing Manager at Pura Vida Bracelets:

“SMS and mobile messaging will overtake all channels as the primary source for people to reach out. Future generations will find ways to take mobile shopping, mobile checkouts, mobile payments to another level through Messenger platforms, texts, live chat, and chatbots.”

“Take a highly aesthetic and digitally native Gen Z movement like VSCO girls. When a VSCO girl laughs it’s ‘SKSKSK.’ It doesn’t sound like laughter. But if you look at your phone keyboard, where are S and K buttons located? Immediately underneath your thumbs. So, ‘SKSKSK’ has replaced ‘LOL’ or ‘Hahaha’ — even though H and A are maybe one or two keys more inside.”

“With social trends influencing buying trends, more and more people will want direct interaction immediately on the places they live — their phones. Hardwired mobile users whose expectations of online shopping won’t be limited to fashion ecommerce stores, ecommerce sites, or online shops.

“They’ll also want to take care of returns and exchanges through those mobile devices. The beautiful thing is the more active you get on those tiny screens, the more proactive you get as someone shops, returns not only get faster but fewer.”

The COVID-19 shutdown did major damage to the fashion industry, causing what some have called an existential crisis. “No-one wants to buy clothes to sit at home in,” said Simon Wolfson, CEO of Next.

Admittedly, this statement could be overblown. The activewear sector experienced a spike in sales during shutdown — an increase caused by the need for comfortable clothes to work and workout in from home.

The point of Wolfson’s statement is that most people aren’t buying clothing or fashion accessories to look good. Since they can’t go out and show off their new duds, many consumers are avoiding fashion-related purchases altogether.

With a surplus of now-out-of-style products, fashion companies are left wondering what to do.

Some have tried offloading old stock via clearance sales and promotional offers. Others have decided to hold and rebrand it for next year. Still, others have looked to expand into different geographic markets where old stock may be more in demand.

Breakout success, however, has come from brands tailoring their approach to the needs of their community.

None illustrate this level of authenticity better than fitness apparel brand, Born Primitive. Like all fashion labels, coronavirus hit Born Primitive hard. March 16th was the single worst day in company history. Within that challenge, however, lay a massive opportunity.

Turned off by standard “work out at home” campaigns, Bear Handlon — Born Primitive’s CEO — organized a 50%-profit-sharing initiative with gyms across the US.

For creative, Bear and Born Primitive’s athletes shot explainer videos, posted them organically, and rapidly scaled spend:

Community-centric initiatives amidst COVID-19 also led to an unlock for wedding and active accessory brand, QALO.

Inspired by healthcare workers within the medical community, QALO responded with the Strata “Pulse” Silicone Ring.

Added to the product was a giveback program; for each purchase of the rings, $10 was donated to Project N95 to help source personal protective equipment to those in need.

Launched at the end of April 2020, the rings quickly sold out in popular colorways. As a result, more than $125k has been donated.

The growth and engagement resulting from the First Responder ring campaign serves as a strong reminder that the core of success comes from supporting your unique customer communities.

So, has coronavirus changed everything?

No. But only because both examples coalesce around a single theme common to all the data and trends we’ve examined …

In the end, the state of ecommerce fashion is good. Evolving? Yes. Risky? Sure. Without challenges? Of course not.

Nonetheless, every source declares: “From biggest to even bigger.”

Common to each trend is the centrality of customers. Seasons change. Tastes transform. Fads come and go.

But people stay people.

Regardless of style … we all want to belong. We all want buying to be easy. And we all want to look good.

Aaron is the VP of Marketing at CTC. Previously the Editor in Chief of Shopify Plus, his content has appeared on Forbes, Mashable, Entrepreneur, Business Insider, The New York Times, and more. Connect with Aaron on Twitter or LinkedIn (especially if you want to talk about bunnies or #LetsGetRejected).