The brands that will come out of this period strongest are not the ones who absorbed every cost increase and hoped for the best. They are the ones who built systems, stayed informed, and moved first when the courts made things right.

There is a number I want you to sit with for a moment: $166 billion. That is the total amount of IEEPA tariff duties collected from 330,000 importers across 53 million shipments between February 2025 and February 2026. The Supreme Court ruled those tariffs unconstitutional. The Court of International Trade ordered CBP to build a refund mechanism. And on April 20, 2026, at 8:00 AM Eastern, that mechanism went live.

Alfred Mai runs ASM Games out of San Francisco. He makes family card games, sources from China, and had every penny of his IEEPA tariffs overturned by the court. On the morning CAPE launched, he recorded himself filing. It took him five minutes to submit claims for 17 shipments totaling more than $160,000. Five minutes.

The merchants who came prepared are getting paid first. The merchants waiting to figure out whether this applies to them are falling further back in the queue every day. This piece is for the ones who want to move.

The IEEPA tariff refund exists because the Supreme Court of the United States ruled, 6 to 3, that the executive branch never had the authority to impose these tariffs in the first place. On February 20, 2026, in Learning Resources, Inc. v. Trump and its consolidated case, the Court held that the International Emergency Economic Powers Act does not authorize the President to impose tariffs, and that tariff authority rests with Congress alone. Every dollar collected under those executive orders was collected without lawful authority.

The decision was categorical on the merits. What it left open was the mechanics of getting money back to 330,000 importers across 53 million entries. That gap is what the Court of International Trade moved to fill. On March 4, 2026, Judge Richard Eaton issued an order in Atmus Filtration, Inc. v. United States directing CBP to stop liquidating IEEPA duties and begin unwinding duties already assessed. The order applied to all importers of record, not just those who had filed suit. Judge Eaton was assigned as the sole judge for all 2,000-plus IEEPA refund cases, and he moved with a speed that surprised most observers.

CBP’s own court filing put the scope in plain numbers: approximately $166 billion collected across 53 million shipments involving 330,000 importers. The outstanding balance is accruing roughly $650 million in interest per month. That interest is included in your refund. Filing early means you are not leaving that accrual on the table.

One thing this refund does NOT cover, and I want to be direct about this: the 10% Section 122 global surcharge that replaced IEEPA on February 24, 2026 is legally distinct and not refundable through CAPE. Neither are Section 232 tariffs on steel, aluminum, autos, and semiconductors, nor Section 301 China tariffs that predate IEEPA. Those all remain in force. CAPE is specifically for the IEEPA-authorized duties that the Supreme Court struck down.

Phase 1 covers two categories of entries: unliquidated entries (those still under active CBP review) and entries liquidated within the preceding 80 days of April 20, 2026. If your entry liquidated after January 30, 2026, you are in Phase 1. If it liquidated before that date, you are in Phase 2, which has no announced launch date but is expected sometime in summer 2026.

Understanding liquidation matters here. Liquidation is the point at which CBP formally finalizes the duty amount on an entry. It typically happens 314 days after the entry date, which means most entries from mid-2025 onward are likely still unliquidated and fully eligible for Phase 1 right now. If you imported heavily in the second half of 2025, your entries are almost certainly in the Phase 1 window.

Phase 1 does not cover entries subject to antidumping or countervailing duties where the Department of Commerce has issued liquidation instructions, entries with suspended or extended liquidation status, warehouse entries, drawback claims, reconciliation entries, entries with open protests, or any entry where liquidation is final. These categories are queued for Phase 2. RSM US has a clear breakdown of the Phase 1 versus Phase 2 scope if you want to dig into the technical distinctions.

There is a strategic point here that I cannot emphasize strongly enough: an accepted CAPE Declaration cannot be amended, and each entry can only appear on one accepted declaration. Merchants with mixed eligibility, some entries in Phase 1 and some in Phase 2, should not dump everything into one CSV and assume CBP will sort it out. A single ineligible entry can cause specific line items to be excluded without recourse. Per Norton Rose Fulbright’s filing guidance, each declaration can include up to 9,999 entries, and multiple declarations are permitted. Use that flexibility. File your clean Phase 1 entries now. Hold your Phase 2 candidates for the next round.

The refund potential for Shopify merchants is real, and it is stage-specific in ways that should inform how urgently you act this week.

To understand the math, you need to know the IEEPA rate structure. The baseline reciprocal tariff was 10% on most countries after April 2, 2025. Vietnam faced 46%. China faced rates up to 145% on certain goods. Canada and Mexico faced separate fentanyl-related tariffs. TariffsTool has a clear breakdown of the IEEPA rate structure by country and category if you need to reconstruct your exposure. A Shopify merchant who imported $500,000 of apparel from Vietnam during the window could be looking at $230,000 in recoverable duties depending on timing and HTS classification. That is not a rounding error in a small business cash flow.

Alfred Mai’s experience at ASM Games is the best-case scenario: prepared, documented, and done in five minutes for $160,000 in claims. Beth Benike at Busy Baby, a Minnesota-based baby products brand, had a different morning. She spent four hours on hold with CBP resolving a duplicate tax ID error before she could file. Both are real operators. The difference was not the size of the claim. It was preparation.

FedEx, UPS, and DHL have publicly committed to passing refunds through to customers who paid tariff fees directly through those carriers. If you shipped via small-parcel services and those carriers acted as your de facto broker, watch for pass-through refund announcements from them. You may not need to file anything at all for those shipments.

For starting-stage merchants doing $0 to $100K: even a single 40-foot container from China with $8,000 to $30,000 in paid IEEPA duties is meaningful recovered capital. Most merchants at this stage are Importers of Record by default and can self-file in under an hour once ACE is set up. The effort-to-return ratio here is exceptional.

For scaling merchants doing $100K to $1M and above: your exposure likely runs into six or seven figures. You almost certainly have a customs broker relationship. Get on the phone with them this week, not next, because broker queues are already filling up. The merchants who are getting processed first are the ones who called on April 21, not May 15.

Filing a CAPE Declaration is more straightforward than the legal backstory might suggest. Here is the workflow from start to submission.

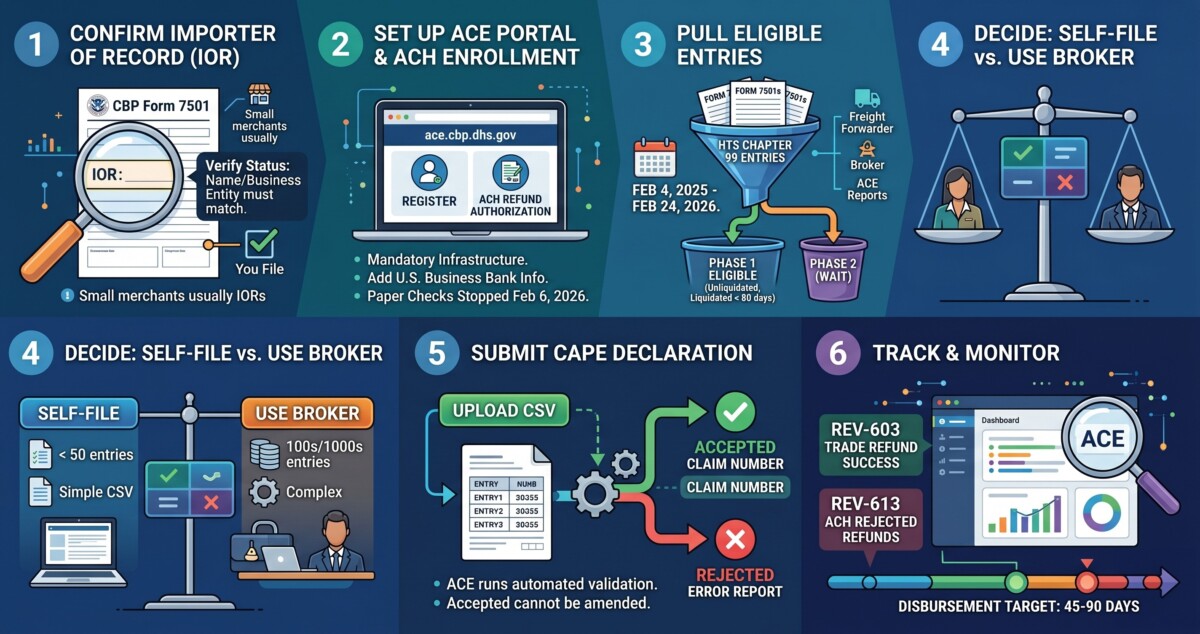

Only the Importer of Record (IOR) or their licensed customs broker can file a CAPE Declaration. Most small Shopify merchants are IORs by default if they handled their own import paperwork. The easiest way to verify is to pull any CBP Form 7501 from the tariff window and check the IOR field. If your name or business entity appears there, you file. Merchants who shipped via FedEx, UPS, or DHL small-parcel services often had those carriers act as broker; in that case, the carrier may file on your behalf. Larger merchants and Shopify Plus brands typically have a dedicated customs broker relationship and should start that conversation now. NerdWallet’s small business tariff refund guide has a clear walkthrough of how to confirm IOR status if you are unsure.

The ACE Secure Data Portal at ace.cbp.dhs.gov is the mandatory filing infrastructure. Merchants without an account can register online in under an hour. After account setup, the critical gate is ACH enrollment: you must use the Importer sub-account to add your U.S. business bank account information in the ACH Refund Authorization tab. CBP stopped issuing paper refund checks on February 6, 2026. Missing ACH information means your refund gets held until you fix it, not rejected permanently, but every week of delay is a week of accruing interest you are not collecting. As of April 14, 2026, 56,497 importers had completed ACH enrollment representing a combined $127 billion in eligible refunds. That number is a fraction of the 330,000 importers who owe. The queue is not crowded yet.

Pull every CBP Form 7501 from February 4, 2025 through February 24, 2026, the full IEEPA tariff window. Filter for entries with HTS Chapter 99 provisions, which is how IEEPA duties are coded on entry summaries. Then separate into two buckets: unliquidated entries and entries liquidated within the last 80 days. Everything in those two buckets is Phase 1 eligible. Everything else waits. If you cannot locate your 7501s, your freight forwarder, customs broker, or accounting system should have them. CBP’s ACE Reports function also lists historical entries tied to your importer account.

Self-filing makes sense when you have fewer than 20 to 50 entries, you are already comfortable in the ACE Portal, your entries are cleanly in the Phase 1 window, and your CSV would be straightforward. Broker-assisted filing makes sense when you have hundreds or thousands of entries across multiple ports, entries are spread across Phase 1 and Phase 2 eligibility requiring careful sequencing, or you have an ongoing broker relationship you do not want to disrupt. Foley and Lardner’s multinational filing guidance has a thorough breakdown of the broker versus self-file decision for more complex situations. A single broker declaration can include up to 9,999 entries across multiple importers, which makes broker filing highly efficient at scale.

Download the CSV template from the CAPE tab inside your ACE Portal account. Fill in the required entry number fields. Upload the CSV. ACE runs two rounds of automated validation: first on the declaration itself (confirming format and that you are the IOR or authorized broker), then on each individual entry (confirming the entry exists in ACE and carries a Chapter 99 IEEPA tariff code). If the declaration is accepted, you receive a CAPE claim number. For invalid entries, the system generates an error report for correction and resubmission. Remember: an accepted declaration cannot be amended. File your clean entries first. Do not rush a messy CSV to beat a queue that does not exist yet.

Once a declaration is accepted, monitor progress through two reports in ACE: the REV-603 Trade Refund report for successful refunds, and the REV-613 ACH Rejected Refunds report for refunds rejected due to missing or incorrect ACH enrollment. CBP’s official CAPE guidance page covers the ACE reporting workflow in detail. CBP’s disbursement target is approximately 45 days post-validation for unliquidated entries, with the broader 60 to 90 day window covering the full processing cycle including compliance review.

The CAPE portal went live on April 20, 2026. Within 72 hours, three patterns were already emerging from early filers. Knowing them in advance will save you hours of frustration.

The first gotcha is duplicate tax ID errors. Beth Benike at Busy Baby hit this one hard, spending four hours on hold with CBP before she could file. The error occurs when multiple entities in the ACE system share a tax ID, which can happen when businesses have restructured, changed names, or had prior accounts created under slightly different entity formats. The resolution requires a direct CBP call. It is not fatal, but it is time-consuming. Check your ACE account status before you need to file, not the day you want to submit. CBS News covered the early filing glitches in detail, including the hold time issues merchants encountered on launch day.

The second gotcha is CSV validation failures. CBP’s two-round validation process flags a range of common errors: wrong entry number format, entries that were never subject to IEEPA duties (no Chapter 99 code), entries outside the Phase 1 window, and entries with suspended or extended liquidation status. Meghann Supino of Ice Miller has advised clients to carefully include all document numbers for forms filed with CBP, because a single bad line can sometimes cause the entire entry to be excluded rather than just the flagged item. NBC Washington’s coverage of the filing process includes specific guidance on CSV preparation that is worth reading before you build your file.

The third gotcha is the broker bottleneck. Customs brokers were already at capacity before CAPE launched. Merchants who assumed their broker would simply handle it are discovering queue times measured in weeks, not days. Fortune’s reporting on the small business challenges with CAPE documents how larger importers with dedicated broker relationships are moving through the queue while smaller merchants wait. If you have a broker relationship, call this week. If you are self-filing, the queue is still manageable right now. Waiting until Phase 2 opens to prepare your Phase 1 entries is a mistake that will cost you months of refund timing.

Getting your refund filed is only the first decision. The second decision, what to do with the 60 to 90 day window while you wait, is where the real financial leverage lives. I have seen this pattern play out across dozens of merchant conversations: the operators who treat a refund as a passive event (file and forget) consistently leave value on the table compared to the ones who treat it as a capital planning moment.

Option 1 is to self-file and wait. No cost, no debt, full refund amount including statutory interest. This is the right choice for most starting-stage merchants and for scaling merchants with healthy cash flow who do not have an immediate capital deployment opportunity. The interest accruing on the refund means the wait is not free money lost. You are earning roughly the statutory rate on the outstanding balance while CBP processes.

Option 2 is borrowing against the refund claim. Commercial banks, hedge funds, and private credit funds are actively lending against CAPE refund claims as collateral, per Fortune’s reporting on importers using refund claims as loan collateral. PYMNTS has covered the mechanics of how businesses are using tariff refund claims as collateral in detail. This gives the merchant immediate cash for operations while preserving the full refund amount. The tradeoff is real: the loan must be repaid regardless of whether the refund comes through on the expected timeline. If the government appeals and a stay is granted, you still owe the loan. Option 2 is worth serious evaluation for scaling merchants with six or seven figures in recoverable duties and a clear capital deployment plan that generates returns above the borrowing cost.

Option 3 is selling the refund rights outright. Financial services firms are purchasing CAPE refund claims at a discount, giving the merchant immediate cash while the buyer assumes the timing and collection risk. This is rarely the optimal choice for a merchant who can wait, because sophisticated counterparties discount heavily. But for a merchant who needs capital now more than they need the full refund amount later, it is a legitimate option.

The decision framework I use with merchants is simple. Starting stage: Option 1 is almost always correct. The refund amount is typically too small to justify the transaction costs of Options 2 or 3, and the interest on the wait is real money. Scaling stage: Option 2 deserves a serious look if you have a proven acquisition channel or inventory opportunity where deploying capital now generates a return above the borrowing cost. The founder who takes Option 2 and deploys the cash into a channel that compounds at 40% annualized may generate more value than the founder who waits 90 days for the full refund and does nothing with the delay. This is the same financial discipline Adam Callinan built into the BottleKeeper playbook and what we explored in depth on Episode 449: The Profit Pyramid. Capital is not just what you have. It is what you do with it while you have the window.

Filing now is the right move, but you should file with a clear understanding of the legal overhang. The U.S. government’s deadline to appeal Judge Eaton’s refund order runs through early May 2026. If an appeal is filed, the refund process could be stayed, potentially delaying all refunds for months or longer. As of this writing, no appeal has been filed, and CBP is proceeding with CAPE as if the order will stand. Skadden’s analysis of the appeal timeline is the most thorough legal read on what a stay would mean in practice.

The practical implication is this: even if the timing shifts due to an appeal, the underlying Supreme Court ruling stands. Eligibility for refunds is not in serious dispute. The only question an appeal touches is the timeline. Merchants who file now and complete ACH enrollment are positioned to receive refunds as soon as processing resumes, whether that is in 60 days or six months.

There is one additional risk worth flagging, particularly for scaling merchants who passed tariff costs explicitly to customers through surcharges or price increases. Class action lawsuits are already underway against retailers including Costco, Lululemon, Temu, Shein, and EssilorLuxottica, arguing that consumers who paid higher prices are entitled to partial refunds from companies that pocketed the duty-inclusive margin. Fortune’s coverage of the small business CAPE challenges touches on this consumer pass-through exposure. If you explicitly passed tariff costs to customers, consult counsel before receiving and keeping the full CAPE refund amount. This is a Tier Two flag in my framework: proceed with filing, but get legal clarity on the pass-through question before the refund hits your account.

The playbook here is stage-specific, and I want to be direct about the urgency for each group.

For starting-stage merchants doing $0 to $100K: if you have ever imported anything into the United States between February 2025 and February 2026, pull your 7501s tonight. Register for ACE Portal access this week. Enroll in ACH. If your volume is low enough that you can self-file, do it yourself before the broker queue worsens. If you imported via FedEx, UPS, or DHL small-parcel, watch those carriers for pass-through refund announcements before you file. You may be able to recover without touching the ACE Portal at all.

For scaling merchants doing $100K to $1M and above: get on the phone with your customs broker this week, not next. Ask specifically about their CAPE filing queue, their fee structure (percentage of recovery versus flat fee), and their timeline for getting your declaration submitted. Have your in-house trade or finance lead pull an inventory of every IEEPA-era entry, categorize by Phase 1 versus Phase 2 eligibility, and build a sequencing plan. Start evaluating whether the 60 to 90 day wait works for your cash position or whether a bridge loan against the refund makes more sense. And if you passed tariff costs through to customers in a way that creates class-action exposure, get counsel involved before the refund lands.

For merchants who think they do not qualify: check anyway. The majority of IEEPA duty payments are eligible for Phase 1. Entries you assumed had already liquidated may still be within the 80-day window. Entries tied to suspended or extended liquidation status are queued for Phase 2. And even if nothing qualifies now, ACE Portal registration is free, takes an hour, and positions you to file the moment Phase 2 opens.

The CAPE refund is significant. But the real lesson for Shopify merchants who import is structural, and it is the one I keep coming back to in conversations with operators at every stage.

The brands that came through the last twelve months strongest were not the ones who got lucky with tariff exemptions. They were the ones who built resilient supply chains before the disruption, diversified their sourcing before they needed to, and maintained the cash reserves and financial discipline to absorb a regulatory shock and keep operating. The CAPE refund is the cleanup round. The operators who will be strongest in 2027 are already asking what the next policy shift looks like and whether their supply chain, pricing, and cash position are built to absorb it.

This is the through-line from the BottleKeeper playbook, from the supply chain conversations across 450-plus episodes of this podcast, and from what I see consistently across the merchants who make it to $2M and beyond. The money you recover through CAPE matters. What you build with it, and what you build against the next shock, matters more.

Your Shopify store qualifies for a CAPE Phase 1 refund if three conditions are met: you paid IEEPA duties between February 4, 2025 and February 24, 2026 (check Form 7501 for HTS Chapter 99 codes), your entries are either unliquidated or liquidated within the 80 days preceding April 20, 2026, and you are the Importer of Record or have a broker authorized to file on your behalf. If all three apply, you are eligible to file now. Merchants who imported via small-parcel carriers like FedEx, UPS, or DHL may have those carriers file on their behalf. Check the CBP official CAPE eligibility page for the most current Phase 1 scope and any updates to Phase 2 timing.

CBP’s disbursement target is approximately 45 days post-validation for unliquidated entries, with the broader refund window running 60 to 90 days from declaration acceptance for the full processing cycle. The clock starts at acceptance, not submission. Refunds include statutory interest. Entries under extended review or flagged for compliance concerns may take longer. Early filers are processed first; the longer you wait to submit, the deeper into the queue you land. NerdWallet’s refund timeline walkthrough breaks down what to expect at each stage of the process.

No. CAPE only refunds duties paid under the IEEPA executive orders invalidated by the Supreme Court’s February 20, 2026 ruling in Learning Resources, Inc. v. Trump. Section 232 tariffs on steel, aluminum, autos, copper, and semiconductors, Section 301 China tariffs that predate IEEPA, and the current 10% Section 122 global surcharge (in effect through July 24, 2026) all remain in force and are not refundable through CAPE. If you are unsure which tariff codes appear on your entries, check Form 7501 for Chapter 99 HTS codes. Great Lakes Customs Law’s working guide on what is and is not refundable is the clearest reference I have found on this distinction.

Self-filing makes sense when you have fewer than 20 to 50 entries, you are comfortable in the ACE Portal, and your entries are cleanly in the Phase 1 window with no mixed eligibility. Broker-assisted filing makes sense when you have hundreds or thousands of entries, entries spread across Phase 1 and Phase 2 requiring sequencing, or an ongoing broker relationship where coordination is already in place. Broker queues are filling up fast as of April 2026, so if you plan to use a broker, call this week. Foley and Lardner’s broker versus self-file analysis covers the decision framework for more complex situations in detail.

If the government files an appeal before the early May 2026 deadline, the Court of International Trade’s refund order could be stayed, potentially delaying all refunds for months or longer. The underlying Supreme Court ruling that IEEPA tariffs were unlawful stands regardless of any appeal on the refund mechanism. Merchants who file now and complete ACH enrollment are positioned to receive refunds the moment processing resumes, whether that is in 60 days or after an appeal is resolved. Filing now does not put your claim at risk. It puts you at the front of the queue when the window reopens. Skadden’s analysis of the appeal timeline and stay risk is the most thorough legal read on the downside scenario.