Retailers absorbed $22 billion in replacement costs and refunds from package theft alone in 2025. That is not a rounding error. It is a line item that has been quietly eroding margins at brands of every size, and most merchants are still handling it manually, one support ticket at a time.

Here is the scenario I hear about constantly from Shopify merchants in the $100K to $500K monthly range. A customer emails saying their package never arrived. The merchant checks the tracking, sees it was marked delivered, and knows from experience that the carrier is going to take six weeks to investigate and probably deny the claim anyway. So they eat the cost, reship the order, and move on. That same scenario plays out dozens of times a month. At $80 to $200 per incident, it compounds into a meaningful drag on margin that never shows up cleanly in the P&L because it hides inside refunds and cost of goods.

The shipping protection category on Shopify has exploded in response to this problem, but most of the apps in it are not actually insurance. They are self-funded protection programs where the merchant collects a small fee at checkout and personally guarantees to cover claims from that pool. That model works well for merchants with low claim rates and high order volume. It works poorly for everyone else, and the regulatory conversation around it has shifted in the last 18 months in a way most merchants have not caught up with.

Parcelis is different. It is backed by actual licensed insurance infrastructure through InsureShip, underwritten by Navigators Insurance Group and The Hartford. That is not a minor distinction. It is the structural difference between a merchant operating a quasi-insurance product without a license and a merchant offering a regulated insurance product through a licensed provider. And the merchant economics, once you understand them correctly, are more favorable than most of the coverage out there suggests.

Parcelis is a licensed shipping insurance app for Shopify that lets merchants offer optional package protection at checkout for lost, stolen, and damaged orders, with the merchant paying a flat $2.50 base per policy, the merchant setting the retail price the customer sees at checkout, and every claim handled by Parcelis rather than the merchant.

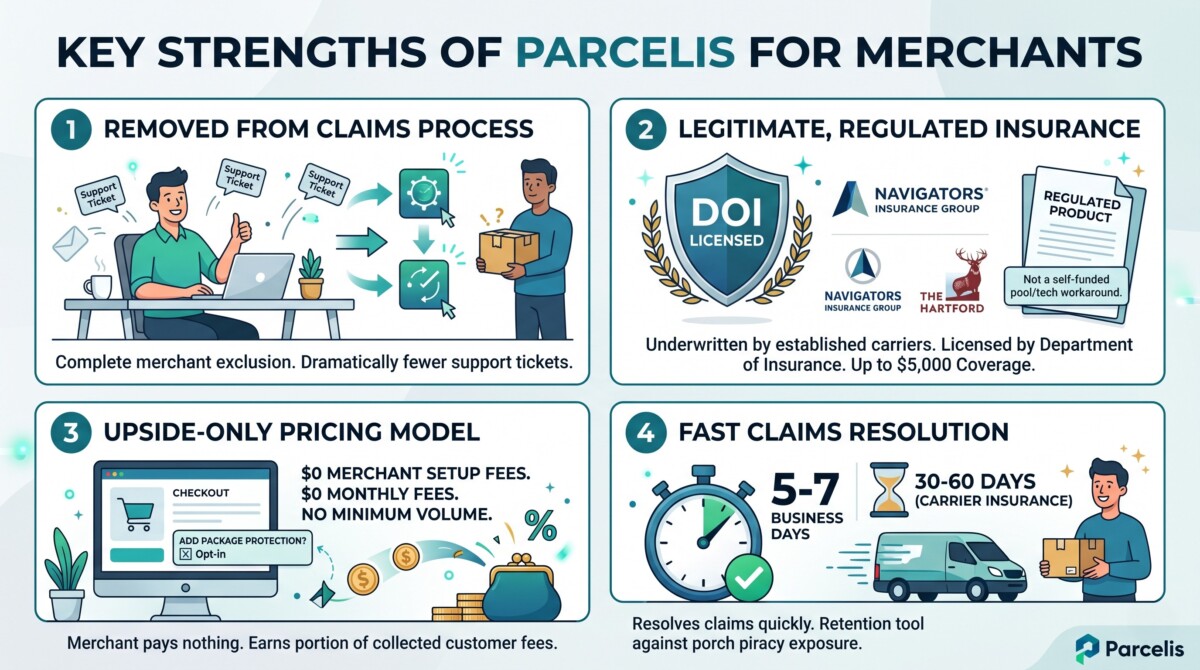

It is not a self-funded protection widget. It is not a carrier claims management tool. It is a checkout-embedded insurance product backed by InsureShip, a licensed insurance agency regulated by the Department of Insurance, with policies underwritten by Navigators Insurance Group and The Hartford. When a customer opts into protection at checkout, they are purchasing a real insurance policy administered by a regulated provider. When they file a claim, they file it through Parcelis’s self-service portal. The merchant is not in the resolution loop at any point.

The economic structure is worth being precise about, because most of the shipping protection coverage online describes this category in terms that do not apply to how Parcelis actually works. Parcelis charges the merchant a flat $2.50 per policy issued. The cost increases by another $2.50 for each additional $200 in cart value. The merchant then sets the retail price the customer pays at checkout. If the merchant charges the customer $4.99 for protection, the merchant keeps the $2.49 difference as margin. If the merchant charges $7.99, the margin is $5.49. This is not a revenue share. It is a price-maker model where the merchant captures the full spread.

Coverage extends to lost packages, damaged shipments, and porch piracy across all major carriers including USPS, UPS, FedEx, DHL, and international carriers. The app installs directly into Shopify, adds a protection widget at the cart page or checkout, and creates automatic policies based on the merchant’s settings. Claims resolve in 5 to 7 business days, compared to 30 to 60 days for standard carrier insurance claims.

Parcelis is best fit for Shopify merchants doing $10K to $500K per month who ship physical goods with any meaningful frequency of loss, damage, or theft claims, and whose average order value is high enough (roughly $60 and above) that a $2.50 per $200 base cost is a small fraction of cart value.

Best fit: Merchants in that $10K to $500K monthly range who are currently eating lost and damaged package costs through refunds and manual reshipping. Merchants in urban and suburban markets where porch piracy rates are elevated and customers already expect protection as an option. Merchants whose support teams are spending meaningful time on “where is my package” tickets and carrier claim follow-ups. Merchants who want a clean margin line on protected orders without absorbing the liability of actually being the insurer. And specifically, merchants who have been running a Navidium-style self-funded program and have started feeling uneasy about the regulatory posture without confirming it with qualified counsel.

Not a fit: Merchants with average order values under $30, where the $2.50 base fee is a large enough percentage of cart value that customer opt-in rates will be weak. Merchants running high order volume (500 plus orders per month) with a documented low claim rate who are profiting meaningfully from the spread on a self-funded model and have a clean compliance review behind them. Merchants who sell primarily digital products. Merchants who need white-labeled branding on the claims portal, since Parcelis operates under its own brand in the claims flow. Merchants who need the protection widget to sit inside a heavily customized checkout extension, as widget placement compatibility should be verified before installing.

Requires: A Shopify store on any plan. No minimum order volume to install, though the economics get more interesting as volume grows. A willingness to set your own retail protection price, since the price-maker model only works if the merchant actually engages with pricing decisions rather than defaulting to a baseline. An expectation that opt-in rates at checkout will determine how many orders are actually covered, with 30 to 45 percent being a realistic range for most stores in this category.

The single strongest outcome Parcelis produces is a real margin line on protected orders, because the merchant sets the retail price the customer pays and keeps the full spread above the $2.50 base cost, without carrying the claim liability that normally comes with that kind of margin capture.

Here is what that looks like in practice. A merchant doing 500 orders per month at $80 AOV, charging $4.99 for protection, at a 40 percent opt-in rate: 200 protected orders per month, $2.49 margin per order, $498 per month in incremental margin with zero claims exposure. That is not transformative revenue on its own, but it is clean margin on orders that already existed, with no operational overhead and no downside scenario where a bad claims month eats the gains. Scaled to 2000 orders per month at the same opt-in rate, the same math produces roughly $2000 per month in margin. At higher AOVs where merchants can charge $7.99 or more for protection, the margin per order doubles.

The second thing Parcelis gets right is the legitimacy of its insurance infrastructure. InsureShip has been operating for over 18 years in the cargo insurance space, is licensed by the Department of Insurance, and is underwritten by Navigators Insurance Group and The Hartford, two of the most established names in commercial insurance. Coverage goes up to $5,000 per shipment. This is not a tech workaround. It is a regulated insurance product with actual risk transfer. For merchants who have been running a self-funded protection program without auditing their position under the National Association of Insurance Commissioners’ guidance (the NAIC issued a public consumer alert in July 2024 flagging that unlicensed entities selling package protection may be operating outside state insurance regulations), this model removes that exposure entirely.

The third strength is the revenue retention story on approved claims. When a covered package is lost or damaged and the claim is approved, Parcelis handles the replacement or reimbursement to the customer. The merchant’s original order revenue stays intact. There is no refund processed against the original order, no chargeback risk, and no “leaky bucket” effect on top-line revenue from disputed shipping incidents. Combined with the reduction in support ticket volume (shipping issues tend to be among the most time-expensive ticket categories), this turns what is currently a quiet margin drain for most stores into a neutral or positive line item.

The fourth strength is claims resolution speed. Carrier insurance claims take 30 to 60 days on average. Parcelis resolves in 5 to 7 business days. For a customer dealing with a lost or stolen package, that difference is the difference between a brand they trust and a brand they never order from again. According to eMarketer research, 44 percent of consumers who have had packages stolen say they now order online less often. A fast, frictionless resolution is a retention mechanism, not just a cost management tool.

Parcelis is free to install with no monthly subscription fee, with the merchant paying a flat $2.50 base cost per policy and a $2.50 increment for each additional $200 in cart value, as of April 2026. The merchant sets the retail price customers pay at checkout, and every dollar above the base cost flows to the merchant as margin.

Value at early stage ($0 to $500K annually): This is where Parcelis produces the clearest ROI for most stores, because the zero-subscription cost structure means there is no fixed overhead to justify and every protected order is incremental clean margin. The honest caveat is that opt-in rates drive everything at this stage. A merchant doing 100 orders per month at a 40 percent opt-in rate with $4.99 retail pricing generates roughly $100 per month in protection margin. That is not going to change the business, but the install cost is nothing, the claims liability is nothing, and the customer experience on the small percentage of orders that go sideways improves meaningfully. Merchants at the lower end of this stage should frame this as a customer experience and operational relief decision first, not a revenue decision.

Value at growth stage ($500K to $5M annually): This is the sweet spot. A merchant doing 500 orders per month at $80 AOV, charging $4.99 retail for protection at a 40 percent opt-in rate, clears roughly $498 per month in pure margin with zero claims exposure. Scaled to 1000 orders at the same rate, that is roughly $996 per month. The support ticket reduction at this stage also starts to produce real dollar value. If your team is spending two to four hours per week on shipping issue tickets at $25 per hour, that is $200 to $400 per month in recovered capacity, on top of the margin line. Combined, this is the stage where Parcelis stops being a small operational improvement and starts being a line item worth paying attention to on a monthly report.

Value at scale ($5M plus annually): At scale the decision gets more nuanced. Merchants at this stage are likely already running a shipping protection program of some kind. If you are on Route, the question is whether giving up the consumer-facing tracking ecosystem is worth capturing more of the margin per protected order directly. If you are self-funded and profitable, the question is whether the compliance and risk-transfer argument is worth the revenue trade-off. Importantly, the regulatory exposure of self-funded programs tends to scale with the size of the brand, because larger programs attract more attention from state insurance regulators. For a $50M brand running an unlicensed protection pool, the risk of a regulatory action or class action filing is materially higher than for a $500K brand doing the same thing. Merchants at this stage should model both the margin comparison and the regulatory risk comparison before making a decision, and should get Parcelis on a direct call to walk through volume-specific pricing assumptions.

The two primary alternatives merchants should evaluate alongside Parcelis are Navidium (stronger for high-volume merchants with documented low claim rates who want to keep 100 percent of collected fees and are confident in their compliance posture) and Route (stronger for merchants who specifically want a consumer-facing tracking app and brand-name protection experience with an established track record, with the trade-off that Route captures more of the protection economics directly).

Navidium is the closest direct alternative on merchant economics. It lets the merchant collect the full protection fee and keep 100 percent of it, paying out claims from that pool. The monthly subscription typically runs from around $10 to several hundred dollars depending on volume. For a merchant doing 1000 orders per month with a 3 percent or lower claim rate, the math on Navidium can beat Parcelis on pure margin per protected order, because there is no base cost to the merchant on the policy side. The two real trade-offs are that the merchant carries all the claims risk directly (a bad month means the merchant pays out of pocket), and that the merchant is effectively running an unlicensed insurance program, which the NAIC flagged publicly in July 2024 as a category where unlicensed entities may be operating outside state regulation. A growing body of class action litigation filed in 2025 and 2026 has targeted protection plan operators on similar grounds, with outcomes still unresolved. Merchants comfortable with that risk and running the model profitably may reasonably stay on it. Merchants who want that risk transferred to a licensed carrier should not.

Route is the closest direct alternative on product experience, though its strategic posture is very different. Route operates as a third-party consumer brand. Customers see Route at checkout, file claims with Route, and interact with the Route consumer app for tracking. For merchants who want a hands-off solution with strong brand recognition and who are willing to trade margin per protected order for operational simplicity and the Route consumer ecosystem, it is a defensible choice. The merchant economics on Route have historically been a source of friction for stores as they have scaled, because Route captures most of the protection fee economics directly. If margin per protected order is a priority and a branded consumer tracking app is not, Parcelis is the better fit.

A few other alternatives worth knowing about: OrderArmor runs a flat-subscription model that some high-volume merchants prefer at scale; ShipAid offers a per-order model similar to Parcelis but with a longer operating track record; and Extend is worth evaluating separately if the underlying need is product warranty rather than shipping protection, since that is a different category with different economics. For most Shopify merchants in the $10K to $500K monthly range evaluating shipping protection specifically, the decision comes down to Parcelis, Navidium, or Route.

For Shopify merchants doing $10K to $500K per month who are currently absorbing shipping losses through refunds and manual reshipping, or who are running a self-funded program without a clean compliance review behind it, Parcelis is worth installing and testing right now, with the honest caveat that it is a new app and you should treat the first 60 to 90 days as a data-gathering exercise.

Here is what I keep coming back to. Most merchants in that range are handling shipping issues the hard way. They are eating the cost of lost packages because carrier claims are a nightmare. They lack a formal protection program, or they have a self-funded one they have not audited. Parcelis solves the operational problem with zero upfront cost and zero claims involvement, and solves the margin problem through a price-maker model that puts real margin on the line where there used to be a quiet drain. The underwriting infrastructure behind it is real. The Hartford and Navigators have been doing this for a combined 300 plus years. The compliance posture is clean in a way that most of this category is not.

The thing I would not do is install this and assume the economics will take care of themselves. This is a product that rewards merchants who actually engage with pricing decisions. Set your retail protection price deliberately for your AOV. Watch your opt-in rate in the first 30 days. Run the margin math honestly against your specific store. If your opt-in rate lands at 40 percent and your AOV is $80 or higher, the numbers work cleanly. If you land at 20 percent opt-in with a $35 AOV, the math is thin and you may want a different approach entirely.

I have not run Parcelis personally. The early merchant reviews are positive but the sample is small. What I can tell you is that the structural model is sound, the compliance foundation is real, and the zero-cost entry makes this a low-risk experiment for any merchant in the fit range who is currently handling shipping losses the hard way. If you are already on Navidium running profitably and you have done the compliance homework, stay with what is working. If you are at $5M plus and evaluating protection programs at scale, get a direct conversation with Parcelis about your specific volume before deciding. But if you are in that $10K to $500K monthly range and you are still handling shipping claims through your support inbox, this is a straightforward install.

Install Parcelis, set your retail price deliberately, run it for 60 to 90 days, and make your long-term decision based on real data from your own store rather than from third-party reviews, including this one.

Parcelis is actual licensed insurance, not a self-funded protection program. It is powered by InsureShip, a licensed insurance agency regulated by the Department of Insurance, with coverage underwritten by Navigators Insurance Group and The Hartford. When a customer purchases protection at checkout, they are buying a regulated insurance policy, not a merchant-backed guarantee. That distinction matters because the merchant is not acting as the insurer and therefore does not carry the compliance exposure that self-funded protection programs do under state insurance regulations flagged in the NAIC’s July 2024 consumer alert.

Parcelis charges the merchant a flat $2.50 base cost per policy issued, plus $2.50 for each additional $200 in cart value. That base cost covers the underwriting, claims handling, and infrastructure. The merchant then sets the retail price customers pay at checkout. If the merchant charges a customer $4.99 for protection, the merchant keeps the $2.49 spread as pure margin. If the merchant charges $7.99, the margin is $5.49. This is a price-maker model, not a revenue-share model: the merchant captures the full spread between the $2.50 base and whatever retail price they choose to charge.

Parcelis covers lost packages, damaged shipments, and porch piracy (theft after confirmed delivery) across all major domestic and international carriers including USPS, UPS, FedEx, and DHL. Coverage goes up to $5,000 per shipment. Standard exclusions apply, including items prohibited by the carrier, packages shipped to freight forwarders, and losses due to improper packaging. Full coverage terms are available through the Parcelis claims portal and InsureShip’s policy documentation, and merchants should review the complete terms before going live.

Customers file claims directly through Parcelis’s self-service portal. The merchant is not involved in the process at any point. Customers submit their claim documentation online, and Parcelis resolves approved claims within 5 to 7 business days. This compares to 30 to 60 days for standard carrier insurance claims. When a claim is approved, Parcelis handles the replacement or reimbursement to the customer directly, which means the merchant’s original order revenue stays intact rather than being refunded.

With Navidium and similar self-funded apps, the merchant collects the protection fee, keeps 100 percent of it, and personally guarantees to cover claims from that pool. The merchant captures all fee revenue but bears all the claims risk and may face regulatory exposure in states that require insurance licensing for protection programs. With Parcelis, a licensed insurer bears the claims risk and handles all resolution, and the merchant captures margin through the spread between the $2.50 base cost and the retail price the merchant sets. The Navidium model can produce more revenue per protected order for high-volume merchants with low claim rates and clean compliance reviews. The Parcelis model transfers the risk entirely and removes the compliance question.

The merchant sets the retail price customers pay at checkout. The merchant’s base cost from Parcelis is $2.50 per policy at cart values up to $200, increasing by $2.50 for each additional $200 in cart value. Merchants can set any retail price above the base cost they choose, and the spread flows directly to the merchant as margin. Most merchants in the category price protection between $2.99 and $9.99 at checkout, depending on their AOV and how aggressive they want to be with the margin line.

Parcelis is listed as working with Shopify Checkout and Shopify Admin, which means it is compatible with standard Shopify plans and Shopify Plus. The widget can be placed on the cart page or at checkout. Shopify Plus merchants using checkout extensibility should confirm widget placement compatibility with Parcelis directly before installing, as checkout customization behavior can vary by theme and Plus configuration. For merchants on heavily customized checkouts, a short compatibility conversation before install is worth the 15 minutes it takes.

At under $20K per month, the monthly margin from Parcelis will be modest, likely in the $50 to $150 range depending on AOV and opt-in rate, but the cost to install is zero and the customer experience and support ticket benefits are real regardless of volume. The stronger case for Parcelis at this stage is operational relief and the ability to offer customers a credible protection option without overhead. If your average order value is above $60 and you ship to urban markets with elevated porch piracy rates, opt-in rates will be meaningful enough to make the program worth running even at low volume.