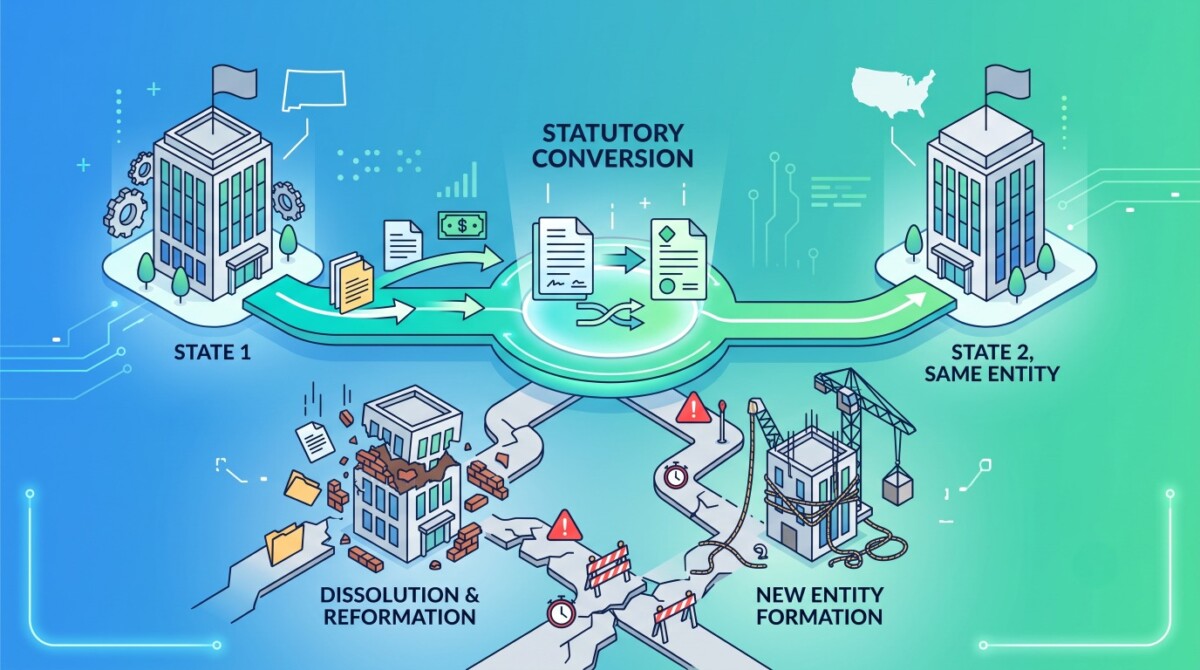

The safest way to move your company to a new state is a statutory conversion, which changes your entity’s legal home while keeping the same business, tax ID, contracts, and history intact. Foreign qualification, dissolution and reformation, and merger workarounds all add risk, complexity, or extra tax exposure without delivering that clean continuity.

Statutory conversion turns moving your company to a new state from a risky entity reset into a controlled change of legal home, but only if you avoid the three common workarounds that quietly keep you tethered to the state you wanted to leave.

For companies based in the United States, a business entity’s state of formation is a variable, not a fixed attribute. It can be a strategic advantage to leapfrog competitors or an albatross hindering future growth. LLCs, corporations, and partnerships formed in one state can be converted to another state’s jurisdiction through a legal procedure called statutory conversion. The entity retains its full legal identity through the transition. Its federal employer identification number, contracts, bank accounts, credit history, intellectual property, ownership structure, capital accounts, and tax elections all survive the filing.

The difficulty is not that the procedure is unavailable. It is that most business owners who search for information on changing their entity’s home state encounter three other procedures first, each of which produces a worse outcome than the conversion they were looking for.

Foreign qualification registers the entity in a second state but does not change its domicile. The company remains subject to every obligation imposed by the original state, including its taxes, annual fees, and regulatory requirements. For entities formed in California, this means continued jurisdiction of the Franchise Tax Board. For entities formed in New York, it means continued exposure to New York’s LLC filing fee and, for New York City entities, the unincorporated business tax. Foreign qualification adds a second set of obligations without removing the first.

Dissolution and reformation terminates the original entity and forms a replacement. The original entity’s contracts are voided. Its FEIN and all associated tax elections are lost. Members or shareholders become personally liable for debts and obligations of the dissolved entity, a category that includes warranties, indemnification commitments, and contingent liabilities that may not be known at the time of dissolution. Both federal and state taxable events are common. The replacement entity begins with no operating history, no credit history, and no legal continuity with the business it replaced.

Merger-based restructuring involves forming a new entity in the target state and merging the original into it. This adds legal fees, dual filing requirements, and the risk that the IRS will not treat the merger as a non-taxable reorganization. If the merger is taxable, the owners face a tax bill for a transaction that produced no economic return. The added cost and complexity produce no advantage over a direct statutory conversion.

Statutory conversion changes the entity’s domicile from one state to another while maintaining its uninterrupted legal existence. The entity is not dissolved, and no new entity is created. The LLC, corporation, or partnership that existed before the filing is the same entity that exists after it. Vendors, customers, and lenders do not require notification. Payroll systems continue without modification. Banking relationships persist under the same FEIN.

When the conversion is part of a coordinated multi-state tax strategy, it can sever the entity’s nexus with the former state. Once nexus is eliminated, the entity has no further obligation to file returns or remit taxes in the jurisdiction it has left. This result is unavailable through foreign qualification, which maintains the entity’s presence in the original state by definition.

The migration of business entities out of high-tax states is not a projection. It is documented. Tesla, SpaceX, and Coinbase have completed or initiated conversion filings out of their prior home states. Chevron moved its headquarters from San Ramon, California, to Houston. ExxonMobil is relocating its legal domicile from New Jersey to Texas. Public Storage left California for Texas. Citadel and Elliott Management have moved operations out of New York. Foot Locker is relocating from New York City to Florida. Larry Page, Sergey Brin, Peter Thiel, Travis Kalanick, Larry Ellison, and Mark Zuckerberg have each departed or initiated the process of moving a company to a new state.

Political signals have confirmed the direction. Zohran Mamdani’s election in New York City, Abigail Spanberger’s gubernatorial win in Virginia, and the qualification of California’s Proposition 40 for the November 2026 ballot have each reinforced the conclusion that tax and regulatory costs in these jurisdictions will increase, not stabilize.

Dallas-Fort Worth has received more than 100 headquarters relocations since 2018. Goldman Sachs plans to grow its Dallas headcount to 5,000. Miami has branded itself as the financial sector’s southern alternative to New York. The destinations are competing for the entities that the origin states are driving away.

An error in the conversion filing, whether in the Plan of Conversion, the member consents, the formation documents, or the sequencing of filings across the two jurisdictions, can produce inadvertent dissolution. This terminates the entity’s legal existence, creates personal liability for every owner, and triggers taxable events at both the federal and state level. The cost of remediation, which involves reinstatement petitions, amended returns, disclosure obligations, and potential litigation, exceeds the cost of a proper conversion by multiples.

Before any filing is submitted, every business owner should verify that investor agreements, lender covenants, professional licenses, and tax elections permit a change in domicile. A conversion that violates a restrictive covenant or licensing condition produces damage that surfaces months after filing, at a point when correction may be impossible.

Cummings and Cummings Law, a flat-fee transactional practice led by Chad D. Cummings, Esq., CPA, has completed more than 500 statutory conversions. “The volume of companies transferring to a new state has increased in every quarter since 2024,” Cummings observes. “The owners who act on the analysis instead of waiting for certainty are the ones who capture the full benefit.”

This transaction demands counsel with competence in multi-state business organizations law, federal tax law, state tax law, and securities regulation.

A statutory conversion is a legal process that changes your company’s state of domicile while keeping the same legal entity, tax ID, contracts, and ownership in place. Instead of dissolving the old entity or merging into a brand new one, you file a structured plan of conversion so that your LLC, corporation, or partnership continues uninterrupted under the law of the new state. That continuity means your banking, payroll, credit history, and intellectual property ownership all carry through, even though the governing business statute has changed.

Statutory conversion replaces your company’s home state with a new one, while foreign qualification simply registers you to do business in an additional jurisdiction without changing where you are domiciled. Under a conversion, your goal is usually to cut tax and compliance ties with the original state as part of a broader nexus strategy. Under foreign qualification, you accept that the original state will continue to tax and regulate you while the new state adds its own requirements on top.

Dissolving and reforming is risky because it destroys your existing entity and all of the legal continuity that makes your history valuable. When you terminate the original company and stand up a new one, contracts do not automatically follow, your FEIN and tax elections are lost, and owners can become personally liable for old obligations that have not fully resolved. The replacement entity also has no operating or credit history, which can make everything from lending to vendor onboarding harder than it needs to be.

If your conversion filings are incorrect or sequenced poorly between the two states, you can inadvertently dissolve the entity you are trying to move and trigger a cascade of problems. Accidental dissolution can create personal liability for owners, force recognition of taxable events at federal and state levels, and require expensive reinstatement petitions, amended returns, and damage control with lenders or investors. In most cases, the remediation costs end up far exceeding what a carefully planned conversion with specialized counsel would have cost at the outset.

Before starting a statutory conversion, you should audit your investor agreements, loan covenants, key contracts, professional licenses, and tax elections to see how they treat a change in domicile. Many documents treat a move to a new state as a major transaction that requires consent or triggers revised terms, so you want those conversations finished before any filings occur. You should also map your current and target states’ tax and regulatory regimes, then work with multi state business and tax counsel to design a conversion plan that both severs old nexus where possible and keeps your operations running smoothly through the transition.